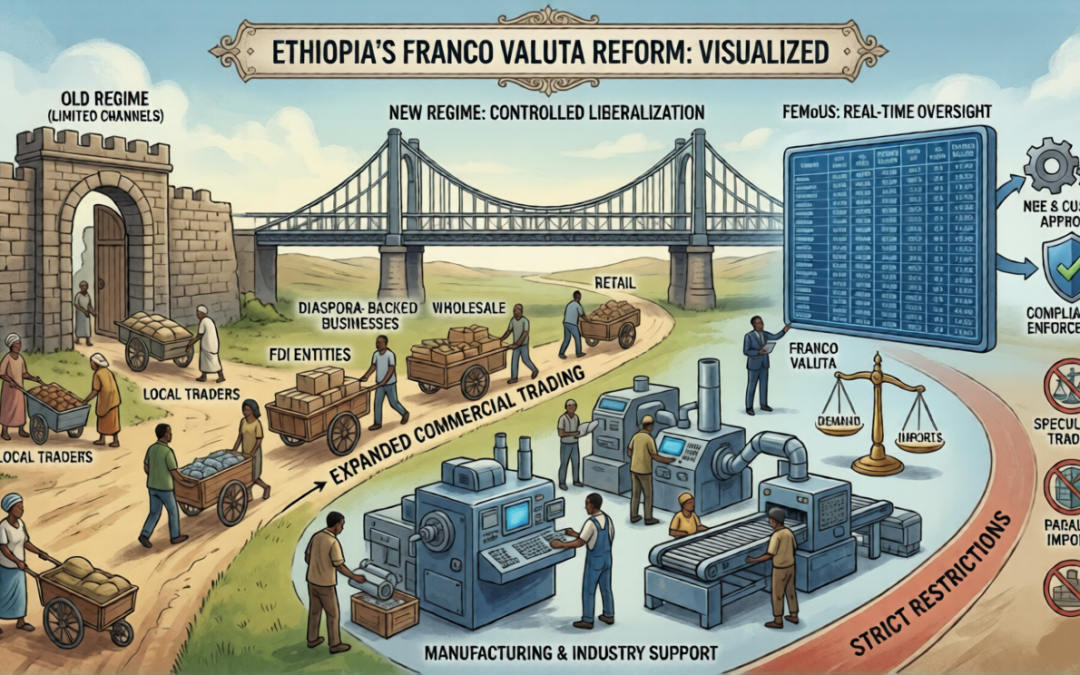

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

The National Bank of Ethiopia has introduced the Import on Franco Valuta Directive No. FVD/01/2026, effective 29 May 2026, establishing a unified and modern regulatory framework governing imports conducted without access to domestic foreign exchange.

Franco Valuta as a Strategic Import Mechanism

Under the new framework, Franco Valuta refers to the importation of goods financed through external or offshore foreign currency sources rather than the domestic banking system. This mechanism is particularly relevant in the current economic environment, where access to foreign exchange remains a key operational constraint for investors, manufacturers, and traders alike.

Trading Imports: Expanded Access Subject to Structural and Regulatory Constraints

The Directive introduces a notable shift by expressly permitting Franco Valuta imports for commercial trading purposes, including wholesale and retail distribution. However, this expansion is carefully circumscribed. In particular, eligibility is limited to foreign direct investment entities and diaspora-backed businesses engaged in domestic trade under applicable licensing regimes, meaning that purely local traders without qualifying investment structures are effectively excluded from utilising this regime for commercial import purposes.

In addition, trading imports remain subject to significant regulatory discretion. Both the National Bank of Ethiopia and the Customs Commission retain authority to review, approve, or reject transactions, particularly where the nature, scale, or frequency of imports raises concerns in relation to foreign exchange management or market distortion. This introduces an inherent approval risk that must be carefully managed at the structuring stage of any trading operation.

Furthermore, the Directive is underpinned by policy objectives aimed at preventing misuse, illicit trade practices, and circumvention of foreign exchange controls. As a result, trading models that replicate parallel import schemes, arbitrage strategies, or high-volume speculative trading are likely to attract heightened scrutiny and may ultimately be restricted or denied approval. This positions Franco Valuta trading not as an open commercial channel, but as a controlled entry mechanism aligned with national economic priorities.

Manufacturing Imports: Strong Policy Support with Embedded Operational Limitations

The Directive provides clear support for manufacturing and industrial activities, recognising their importance in driving economic growth and reducing import dependency. Manufacturers are permitted to import capital goods, machinery, spare parts, raw materials, and industrial inputs under Franco Valuta arrangements, thereby enhancing their ability to maintain production continuity and expand operational capacity.

However, this support is paired with strict limitations aimed at ensuring that imports remain closely tied to genuine production needs. In particular, all manufacturing-related imports must be purpose-driven, meaning that goods must be demonstrably linked to approved investment activities, production processes, or operational requirements. Imports that fall outside this defined scope are unlikely to qualify under the regime.

Quantitative controls further reinforce this limitation. The Directive contemplates that raw materials and inputs will be permitted only in quantities aligned with commissioning stages, pilot production, or actual operational demand, rather than allowing unrestricted or speculative stockpiling. This introduces a requirement for close alignment between import planning, production scheduling, and regulatory compliance.

Additionally, manufacturing entities are subject to rigorous licensing and documentation requirements, including the obligation to maintain valid investment or trade licences and to submit comprehensive supporting documentation, such as invoices, shipping records, and related transactional evidence. These requirements are reinforced by the Directive’s emphasis on auditability, obliging businesses to maintain records capable of withstanding regulatory review at any time.

Digital Oversight and Continuous Compliance

A defining feature of the new regime is the introduction of the Foreign Exchange Monitoring and Orchestration Unified System (FEMoUS), which requires all Franco Valuta transactions to be digitally recorded and monitored. This represents a structural shift from periodic compliance to continuous, real-time oversight. For businesses, this means that regulatory visibility is significantly enhanced, reducing the scope for informal practices and increasing the importance of accurate reporting and internal compliance controls.

Enforcement Environment and Risk Exposure

The Directive establishes a stringent enforcement framework, expressly identifying misuse of Franco Valuta privileges, false declarations, and attempts to circumvent foreign exchange controls as violations. The associated sanctions are substantial, including monetary penalties, confiscation of goods, and potential criminal liability under applicable laws.

In practical terms, this elevates compliance risk to a central commercial consideration. Businesses operating under Franco Valuta arrangements must therefore ensure that their import structures, documentation, and operational practices are fully aligned with regulatory requirements, as failures can result not only in financial loss but also in business disruption and reputational exposure.

Strategic and Commercial Implications

The Directive introduces a carefully balanced framework that simultaneously expands opportunity and imposes discipline. On the one hand, it creates a viable alternative to foreign exchange-dependent imports, enabling businesses to structure transactions using external currency sources and thereby maintain operational continuity. On the other hand, it embeds clear limitations—particularly in relation to trading eligibility, manufacturing scope, and import quantities—that require businesses to adopt a more structured, compliance-driven approach.

From a commercial perspective, the regime favours well-capitalised and strategically organised investors who are capable of aligning their operations with regulatory expectations. Conversely, opportunistic or loosely structured trading models are likely to face significant barriers to entry and increased enforcement exposure.

Our Perspective

The Franco Valuta Directive is best understood as a model of controlled liberalisation, designed to facilitate investment and production while restricting activities that may undermine foreign exchange stability. Its effectiveness will depend not only on regulatory enforcement but also on how market participants adapt their structures and strategies in response.

In this environment, success will depend on the ability to integrate legal, regulatory, and commercial considerations at the earliest stages of business planning. The Directive does not eliminate constraints—it redefines them, creating a system where precision, structure, and compliance are the key drivers of competitive advantage.

How Ethio Alliance Advocates LLP Supports Clients

Ethio Alliance Advocates LLP provides integrated, commercially focused legal advisory services across the full lifecycle of Franco Valuta transactions. This includes structuring compliant trading and manufacturing models, advising on investment and licensing frameworks, managing regulatory approvals, and ensuring alignment with documentation and audit requirements. The firm also advises on cross-border transaction structuring, foreign exchange strategy, and risk mitigation, as well as representing clients in enforcement proceedings and disputes arising under the new regime.

Conclusion

The Franco Valuta Directive No. FVD/01/2026 introduces a powerful but tightly regulated mechanism for importing goods into Ethiopia. While it opens meaningful opportunities for investors, manufacturers, and diaspora-backed trading businesses, it simultaneously imposes a framework of targeted limitations that require disciplined execution.

In this evolving regulatory landscape, the distinguishing factor will not be access to the regime, but the ability to navigate it effectively.

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

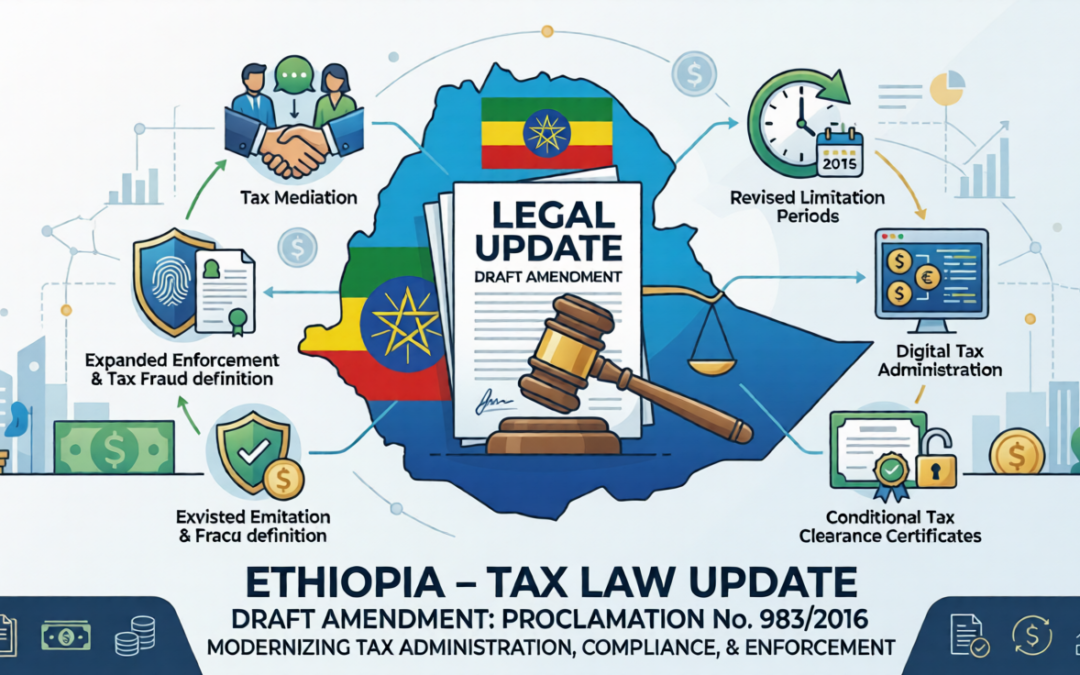

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

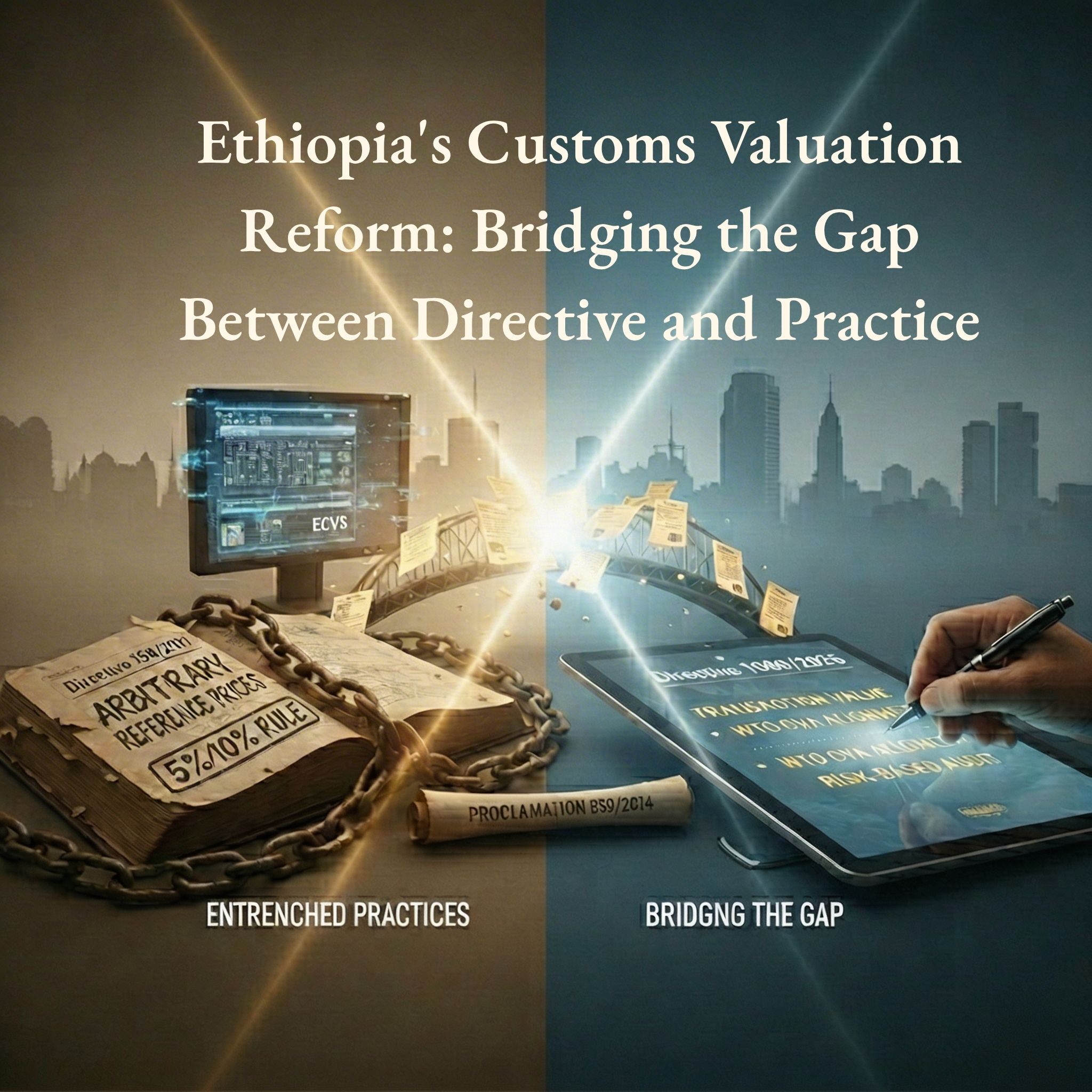

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

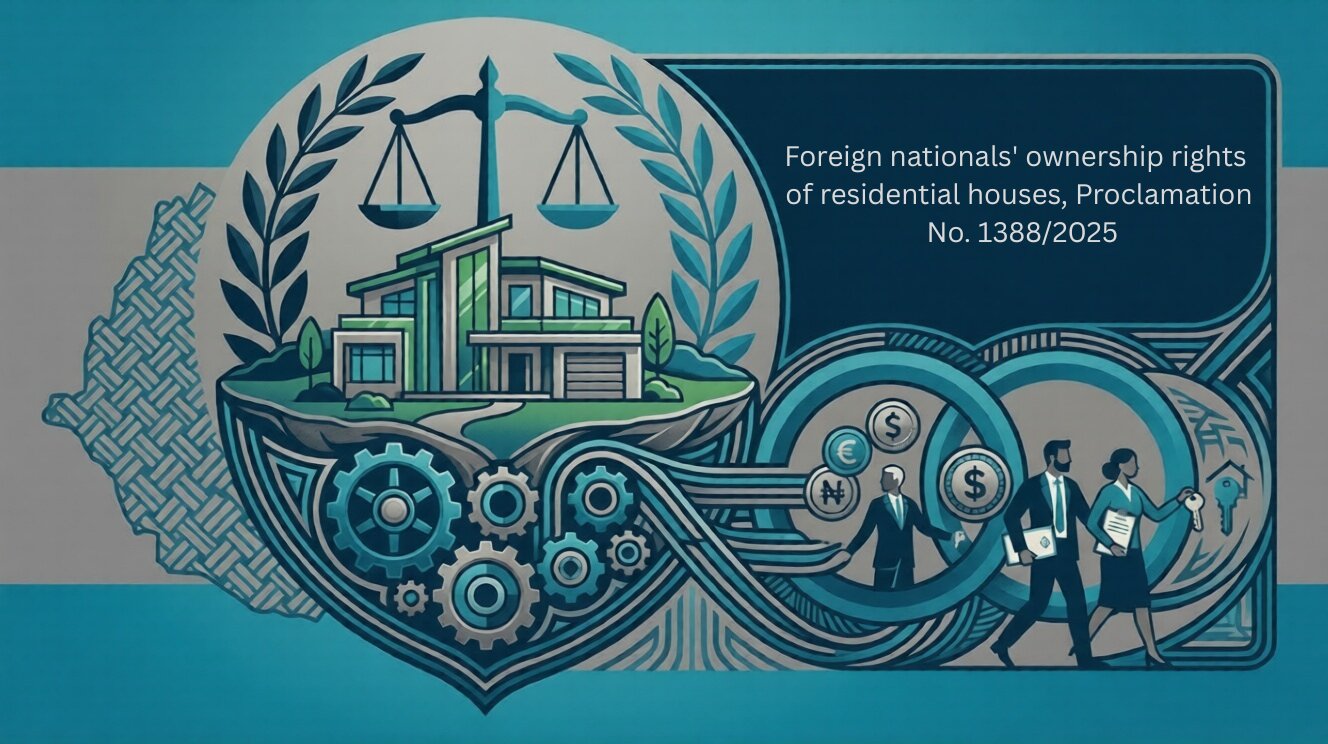

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.

U.S. International Tax Law in a Coffee Bean

The highlands of Ethiopia are widely regarded as the birthplace of coffee. The story of Ethiopian coffee dates back to around 850 AD, when both Arabica and Robusta coffee are believed to have originated. Today, Ethiopia remains the top coffee producer in Africa, cultivating over 5,000 varieties. Coffee is a major global export for the country, where agriculture remains a key driver of the economy. Ethiopia also ranks first in wheat production and third in maize production across Africa.