Legal updates and Recommendations on the Draft Real Estate Bill in Ethiopia

Introduction

The draft bill on Real Estate Development, Marketing, and Property Valuation has been tabled before the House of Peoples’ Representatives (HPR) for ratification following discussions by the Council of Ministers. This legislation is crucial for addressing the challenges faced by the real estate sector, with the goal of ensuring affordable housing. In addition to this, the draft proclamation seeks to regulate several key areas in the interest of the public, developers, and homebuyers. However, there are concerns regarding the lack of regulation on certain issues and the insufficiency of existing laws. This paper aims to highlight the contents of the draft proclamation as a legal update and point out areas of concern that should be reconsidered during the ratification process.

Why the Bill?

As inferred from its preamble, the bill has legal, economic, social, and political justifications.

The primary legal objective of the bill is to establish standards in a sector that has remained unregulated since the inception of real estate development in Ethiopia. The lack of a uniform legal framework has created the need for this bill to set the groundwork for regulating real estate development, property valuation, and real property transactions.

From an economic standpoint, the bill aims to benefit property owners by enabling them to understand the value of their assets, thereby facilitating their participation in capital markets. Additionally, it seeks to boost city revenues nationwide by introducing property valuation standards and levying property taxes, thus contributing to rapid urban growth. The bill also promotes the expansion of the real estate business.

Socially, the bill addresses the ongoing challenges caused by the imbalance between housing demand and supply. It aims to promote real estate development to enhance housing availability. Moreover, the bill seeks to regulate the relationship between developers and homebuyers by institutionalizing a government regulatory body to oversee this dynamic.

Politically, regulating the real estate sector through a government body ensures housing availability and fosters mutually beneficial relationships within the industry. This approach would also contribute positively to the broader political framework by promoting business growth and meeting public needs in this specific area.

Eligibility for Real Estate Development

Under the draft proclamation, both local and foreign investors are permitted to participate in the real estate business in Ethiopia. To qualify, they must obtain a real estate developer’s qualification license from the federal, state, or city-level urban and infrastructure authority. Additionally, to become licensed real estate developers, both local and foreign investors are required to develop a minimum of 50 units per project.

Local investors must also demonstrate the sources of their income before commencing operations. For those interested in presale activities, a presale license from the appropriate authority is required. Foreign investors, in addition to fulfilling minimum capital requirements under the Ethiopian investment proclamation, must submit comprehensive project studies, construction schedules, and other relevant documents.

Article 5(5) of the draft proclamation allows local and foreign investors to engage in joint real estate development projects. However, the proclamation defers the regulation of certain details to forthcoming regulations.

The draft law currently does not address the position of developers producing fewer than 50 units. This includes the nature of their relationships with buyers and the government, as well as the potential benefits or incentives for those contributing to housing supply on a smaller scale. Notably, smaller developers play an essential role in filling the housing demand gap, promoting investment growth, and expanding the industry.

The omission of a framework for sub-50-unit developers is concerning, as prior drafts attempted to address this issue. There is a pressing need for a provision to clarify the standing of smaller developers before the bill’s ratification to mitigate potential legal and operational challenges. A thorough study of the implications for smaller-scale developers is recommended, examining legal, economic, social, and political factors to create a balanced approach.

Access to Land

Under Article 5(4) of the draft proclamation, certain eligibility criteria must be met to qualify for land access. These criteria include the number of housing units to be constructed, reinvestment of remittances in the country of origin, and establishment of factories to substitute imports. Developers building between 500 and 5,000 units at a time and reserving 40 percent of these units for low- and middle-income communities will receive favorable consideration for land access. This provision also applies to foreign investors who reinvest 60 percent of their remittances in their home country or establish factories that reduce dependency on imported construction materials. When investors meet these requirements, the government commits to facilitating favorable conditions for land access.

Article 6 grants priority land access to developers who meet specific unit thresholds: those building over 5,000 units in Addis Ababa, more than 1,000 units in high-demand urban areas and around industrial parks, and over 500 units in smaller cities with lower housing needs. Investors meeting these conditions are given priority rights to access land resources.

However, given the scarcity of land, a thorough analysis is necessary to ensure that land use remains fair and transparent. This approach would help assure equitable and efficient distribution of land resources.

Pre-Sale Rights

The draft bill lacks a dedicated provision specifying who has the exclusive right to conduct pre-sale arrangements. In previous drafts, Article 6(5) established that only local investors could engage in pre-sales. However, that draft first outlined the requirements for local investors to participate in pre-sales before clearly defining their exclusive rights, which created practical issues. To address this, a single, separate provision is necessary to clarify pre-sale entitlements. Additionally, a sub-article should address the implications of pre-sale arrangements in cases of joint investments between local and foreign investors. Without these clarifications, there is potential for confusion-specifically, whether foreign investors acquire pre-sale rights by partnering with local investors, or whether local investors lose such rights when collaborating with foreign partners.

Another important issue to consider is why foreign investors are not entitled to pre-sale rights. The draft explanatory note provides no explanation or rationale for this exclusion. However, the underlying intention of the bill appears to be that foreign investors should bring in capital in foreign currency from their own resources or financial institutions to benefit the country’s economy. Additionally, the bill asserts that foreign investors cannot mobilize public resources, which are reserved for local investors.

Nevertheless, one could argue that foreign investors should be allowed to engage in pre-sales, especially since the primary objective of the law is to increase housing availability. Foreign investors offer skilled labor, technology, expertise, and other industry advantages. Therefore, the country should facilitate pre-sale arrangements for foreign investors under the same restrictions and conditions that apply to local investors. This approach would likely yield no adverse consequences, as funds collected from pre-sales could be deposited in banks and released under the supervision of the appropriate regulatory body.

Another critical point to consider is the issue of contractual fairness between sellers and buyers concerning pre-sale agreements. Although the law attempts to address contractual conditions, it fails to clarify the nature of real estate contracts. The drafters have not adequately addressed the practical challenges associated with categorizing pre-sale agreements as either construction contracts or sales of immovable property.

Understanding the implications of this classification is essential, as it affects the rights and obligations of both parties. If a pre-sale agreement is considered a construction contract, it must meet specific legal criteria associated with such contracts. However, the draft law does not sufficiently explore whether pre-sale agreements fulfill these elements or the potential complications that may arise from this classification.

Additionally, a deeper analysis is needed to determine whether pre-sale agreements should be subject to specific formality requirements to ensure contractual fairness. The law mandates that developers provide various documents, which should be supported by a written contractual agreement. In this context, the drafters must be mindful of the realities on the ground, as the practicalities of the market can significantly impact the effectiveness of these requirements.

The drafters should strive to develop tailored solutions that balance the interests of all contracting parties, taking into account both the type of contract involved and the necessary formality requirements. This approach will help ensure that pre-sale agreements are equitable and practical, fostering a fair relationship between sellers and buyers.

Obligations of the Parties

The draft bill outlines the obligations of each party involved in real esate agreements. Developers are required to provide essential documents, including building descriptions, architectural designs, title deeds, and any other relevant construction documents. They must also issue receipts for payments received from buyers.

In addition to these responsibilities, developers are prohibited from engaging in false advertising and from collecting payments or registering properties before obtaining land ownership and building permits. Furthermore, they are restricted from registering more units than the housing accommodations available. Developers are also encouraged to promote the formation of customer associations to foster better communication and collaboration with buyers.

Buyers have specific obligations under the draft bill, including the timely payment of amounts due and a duty to cooperate by providing necessary information and documentation throughout the contracting process. Additionally, clients are expected to participate in home buyers associations.

Regarding home buyers associations, the responsibilities for their establishment and operation involve a triangular relationship among the buyer, the seller, and the relevant government body. This relationship is inferred from Articles 8(3), 7(5), and 10(2) of the draft bill, highlighting the collaborative role each party plays in ensuring the effective functioning of these associations.

Another important aspect to address is the certification of individual ownership. According to Articles 6(2) and 7(1) of the draft bill, a unit can only be sold once it is 80 percent completed. Transfer of ownership below this threshold is prohibited unless there is mutual agreement between the buyers and the developer. Additionally, upon reaching the 80 percent completion mark, the developer is entitled to request a title deed from the appropriate government authority.

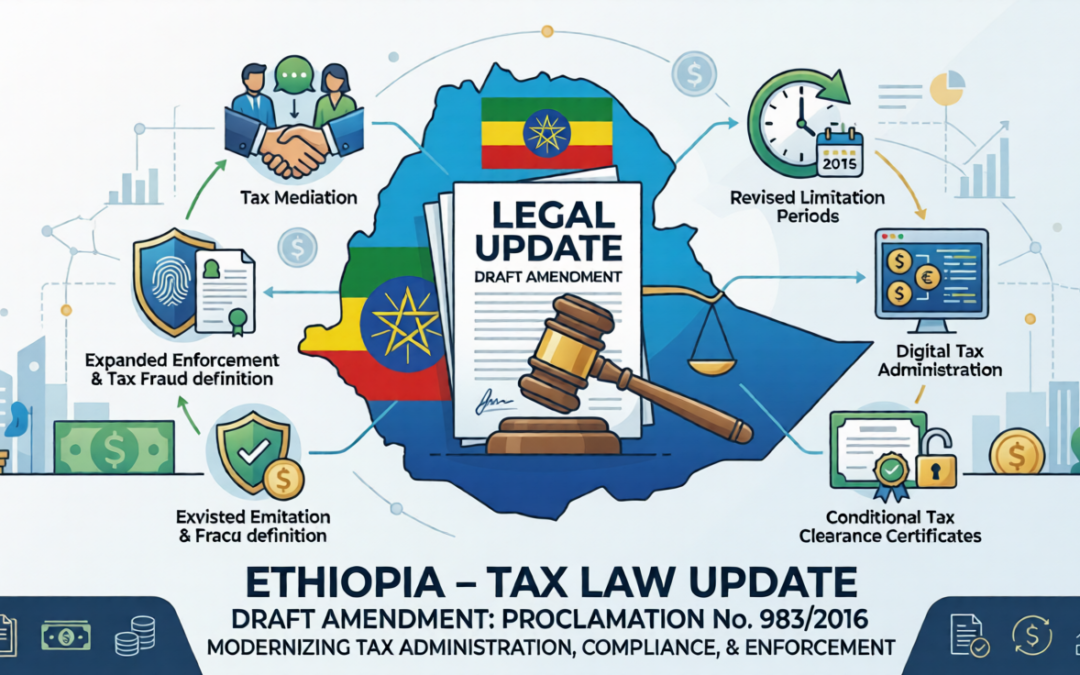

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

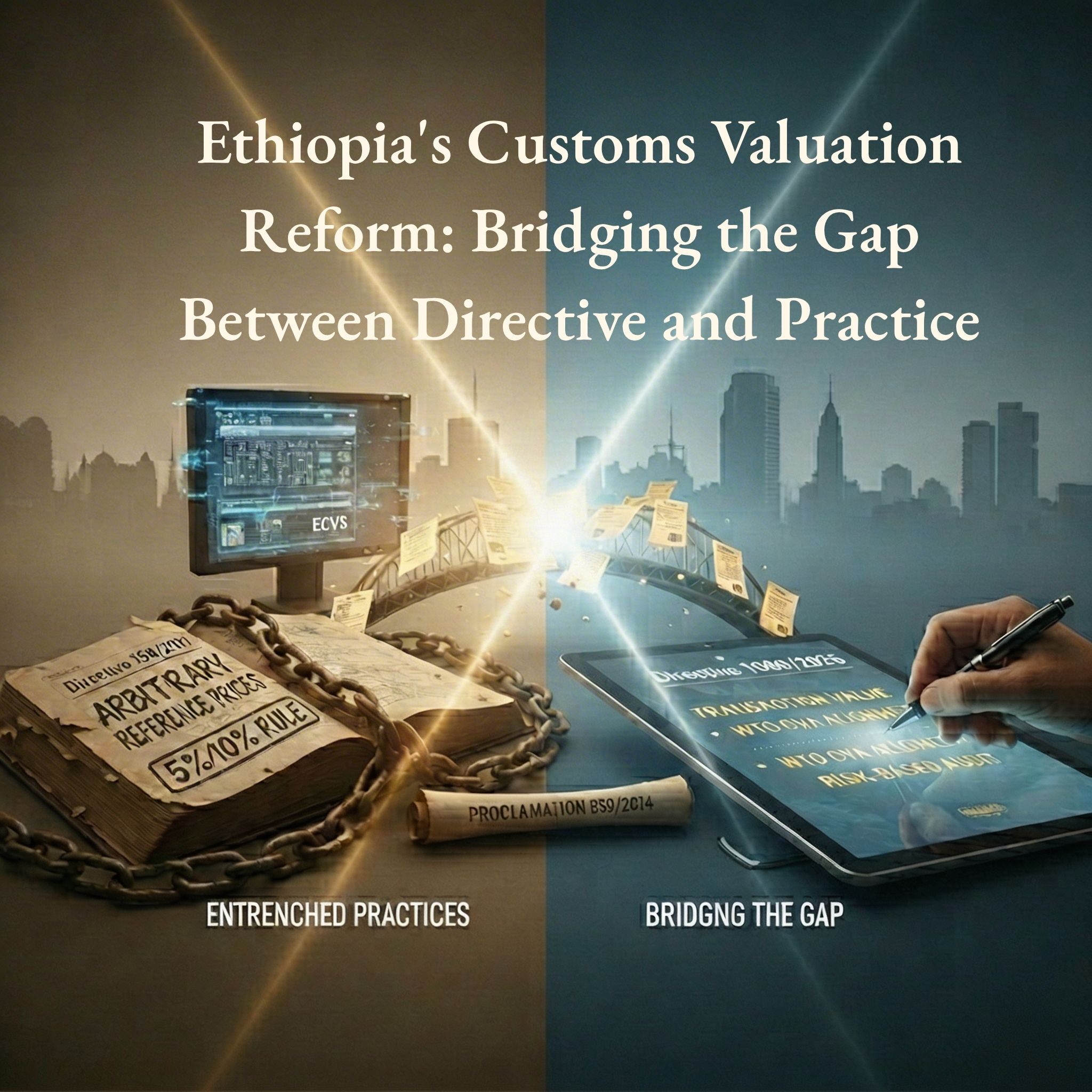

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

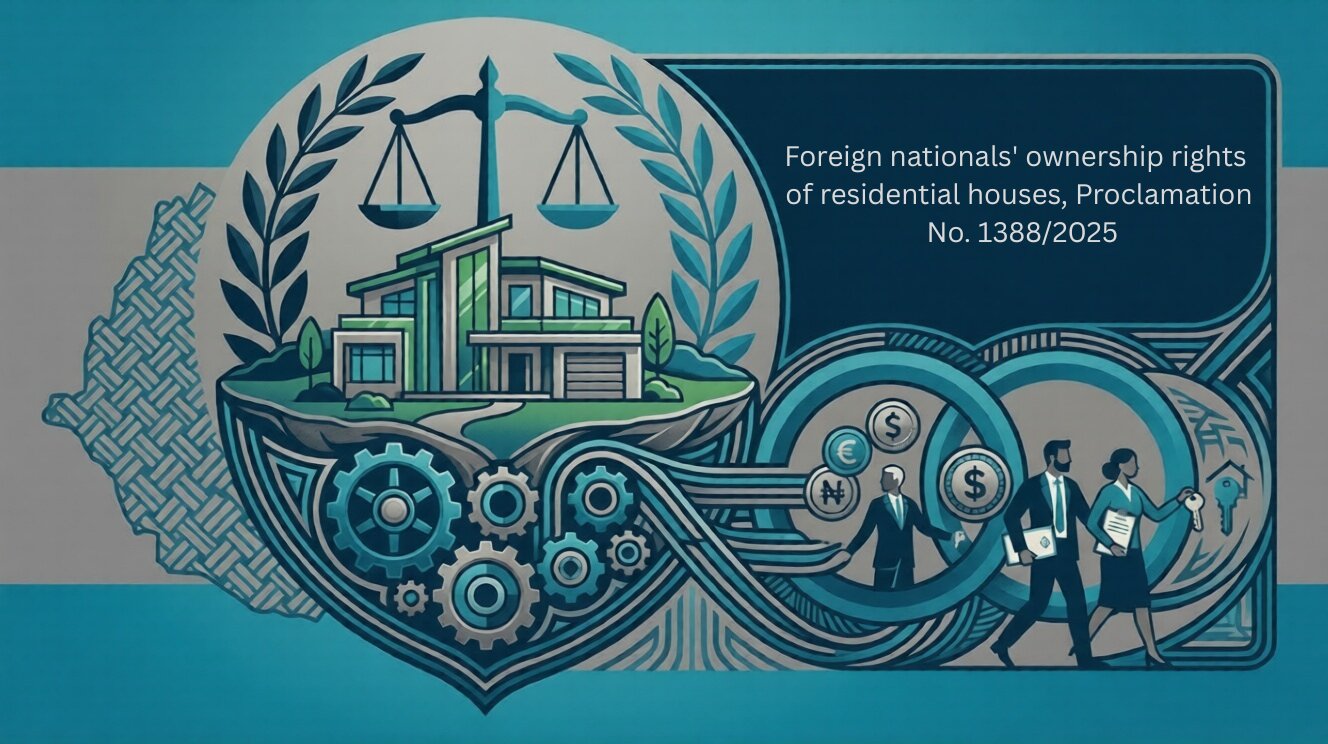

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

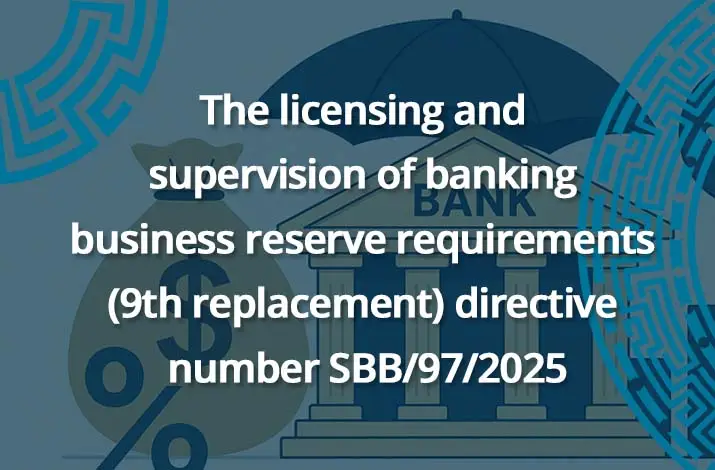

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.

U.S. International Tax Law in a Coffee Bean

The highlands of Ethiopia are widely regarded as the birthplace of coffee. The story of Ethiopian coffee dates back to around 850 AD, when both Arabica and Robusta coffee are believed to have originated. Today, Ethiopia remains the top coffee producer in Africa, cultivating over 5,000 varieties. Coffee is a major global export for the country, where agriculture remains a key driver of the economy. Ethiopia also ranks first in wheat production and third in maize production across Africa.