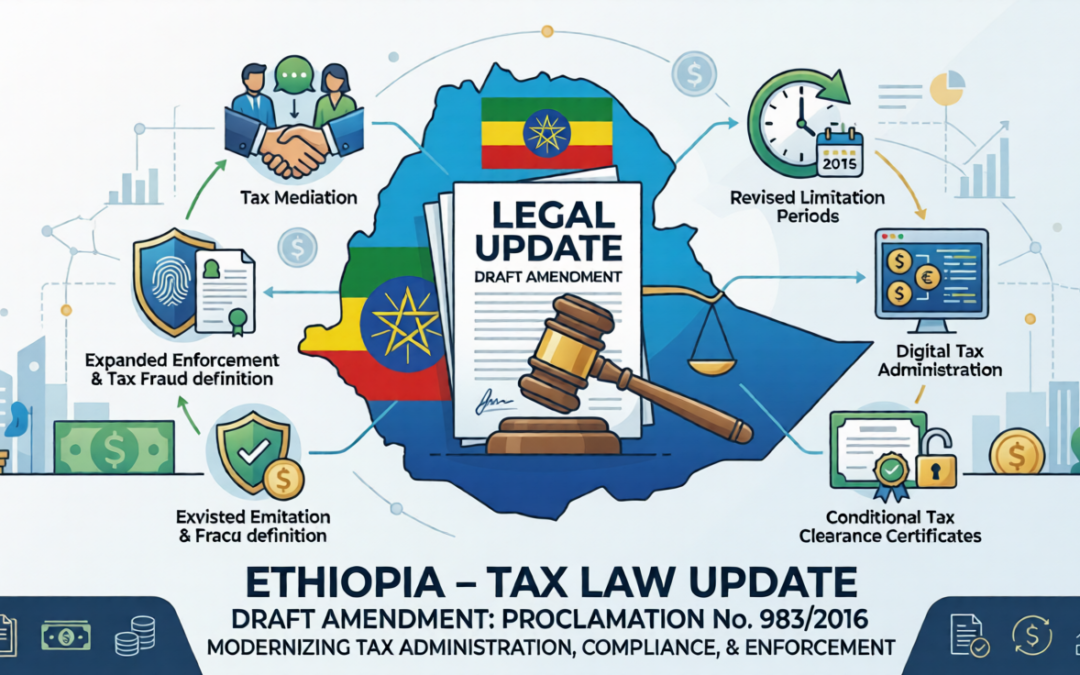

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

Overview

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

The proposed amendment represents a significant evolution of the existing regime, reflecting the Government’s objective to enhance administrative efficiency, strengthen tax compliance, and align Ethiopia’s tax administration framework with emerging international standards. The reforms introduce both procedural modernisation and expanded enforcement mechanisms, with important implications for domestic and multinational taxpayers.

Background

Proclamation No. 983/2016 provides the legal foundation for the administration of Ethiopia’s tax system, covering key areas including taxpayer registration, tax assessments, collection and recovery, dispute resolution, penalties, and enforcement powers.

The draft amendment seeks to address practical challenges observed under the current framework, particularly in relation to dispute resolution delays, evidentiary issues, audit limitations, and the need for digital transformation.

Key Reforms Introduced by the Draft Amendment

1. Introduction of Tax Mediation (Alternative Dispute Resolution)

The amendment introduces, for the first time, a formal tax mediation mechanism as part of Ethiopia’s dispute resolution framework. This mechanism allows taxpayers and the tax authority to resolve disputes through a structured, voluntary process supported by a neutral third-party mediator.

Mediation is designed to operate alongside the existing objection and appeal system, which currently includes administrative review and appeals to the Tax Appeal Commission and the courts.

Mediation is not available in circumstances where the dispute involves suspected tax fraud, where any proposed settlement would be inconsistent with applicable tax laws or the Constitution, or where either the taxpayer or the tax authority does not provide consent to participate in the mediation process.

This reform is expected to:

- Reduce the cost and duration of tax disputes

- Promote cooperative engagement between taxpayers and the tax authority

- Improve efficiency in resolving complex tax matters

2. Expanded Definition and Enforcement of Tax Fraud

The amendment introduces a more comprehensive statutory definition of tax fraud and evasion, including conduct such as:

- Submission of false or misleading documents

- Concealment of taxable income or transactions

- Issuance or use of fraudulent invoices

The existing Proclamation already provides for criminal sanctions, including imprisonment and financial penalties for fraudulent conduct and unlawful invoicing.

The expanded definition strengthens the legal basis for enforcement and reduces interpretive uncertainty in tax investigations and disputes.

3. Revised Limitation Periods and Assessment Powers

The amendment refines the rules governing tax assessments and reassessments, including limitation periods applicable to the tax authority.

Under the existing framework, the authority may amend assessments within five years, except in cases involving fraud or wilful default the assessment conducted at any time, where reassessment may occur with 5 years or additional one year from the tax assessment periods.

The draft amendment:

- Clarifies and expands reassessment powers in fraud cases for ten years

- Provides additional flexibility where new evidence arises

- Enhances the authority’s ability to ensure accurate tax liability determinations

These changes are likely to increase audit exposure and extend the period during which taxpayers may be subject to review.

4. Restrictions on Submission of New Evidence in Disputes

A significant procedural reform is the introduction of stricter rules on the admissibility of new evidence at objection and appeal stages.

As a general principle:

- Taxpayers will be limited in their ability to submit new evidence after the initial assessment stage

Exceptions apply only in narrowly defined circumstances, including:

- Evidence that was not reasonably obtainable earlier

- Evidence arising after the original assessment

- Situations where exclusion would cause material injustice

This reform places greater emphasis on:

- Proper record keeping

- Timely submission of documentation during audits

- Proactive tax risk management

5. Taxpayer Segmentation and Risk-Based Administration

The amendment introduces provisions allowing the tax authority to classify taxpayers based on economic sector or risk profile, consistent with international industry classification standards.

This development supports a shift toward:

- Risk-based audit selection

- Targeted compliance strategies

- Differentiated taxpayer services

6. Conditional Tax Clearance Certificates

The amendment introduces a new concept of conditional tax clearance certificates, allowing taxpayers to obtain tax clearance even where outstanding liabilities exist, provided that:

- A dispute or appeal is pending; or

- A formal payment arrangement has been agreed

Under the existing regime, tax clearance certificates are required for key commercial activities, including licence renewals and public procurement participation.

This reform is expected to:

- Improve business continuity

- Reduce operational disruption

- Facilitate access to finance and investment

7. Expansion of Digital Tax Administration

Building on existing provisions that allow electronic filing and communication, the amendment further strengthens the legal framework for digital tax administration.

Key developments include:

- Increased use of electronic tax systems

- Introduction of e-invoicing mechanisms

- Enhanced monitoring of digital transactions

This reflects Ethiopia’s broader strategy to modernise tax collection and improve transparency through technology.

8. Strengthening Penalties and Compliance Enforcement

The amendment introduces stricter administrative and criminal consequences for non-compliance, particularly in relation to:

- Failure to issue invoices

- Manipulation of invoice values

- Misreporting of tax liabilities

The existing Proclamation already provides significant penalties, including fines and imprisonment for offences such as false declarations, fraudulent invoicing, and tax evasion.

The proposed changes increase both the scope and severity of enforcement measures.

9. Enhanced Powers for Correction of Tax Decisions

The amendment introduces clearer rules for the correction of tax decisions, enabling the tax authority to revise assessments where:

- Errors in calculation or application of the law are identified

- New or previously unavailable evidence is presented

This reform ensures greater accuracy in tax determinations while maintaining procedural safeguards.

10. Cross-Border and Investment-Related Compliance

The amendment introduces additional requirements affecting foreign investors, including:

- Mandatory tax verification prior to repatriation of profits or capital

- Increased scrutiny of cross-border payments

These changes reinforce tax compliance in international transactions and align with global transparency standards.

Practical Implications for Businesses and Investors

The proposed amendments will have significant implications for taxpayers operating in Ethiopia. Key considerations include:

- Enhanced documentation requirements: Taxpayers must ensure that all relevant evidence is prepared and submitted at the audit stage

- Increased audit risk: Expanded assessment powers and longer limitation periods increase exposure

- Strategic use of mediation: Businesses should consider ADR mechanisms as part of their dispute resolution strategy

- Digital readiness: Systems should be aligned with evolving e-invoicing and electronic reporting requirements

- Governance and compliance: Internal controls should be strengthened to mitigate risks of penalties and enforcement action

Conclusion

The draft amendment to the Tax Administration Proclamation represents a major reform of Ethiopia’s tax administration regime, balancing modernisation and efficiency with stronger enforcement and compliance measures.

The introduction of tax mediation, enhanced audit powers, and digital tax mechanisms signals a clear shift toward internationally aligned best practice. At the same time, stricter rules on evidence and expanded penalties underscore the importance of robust tax governance.

Businesses and investors should proactively assess the impact of these reforms and take appropriate steps to ensure compliance and manage tax risk in Ethiopia.

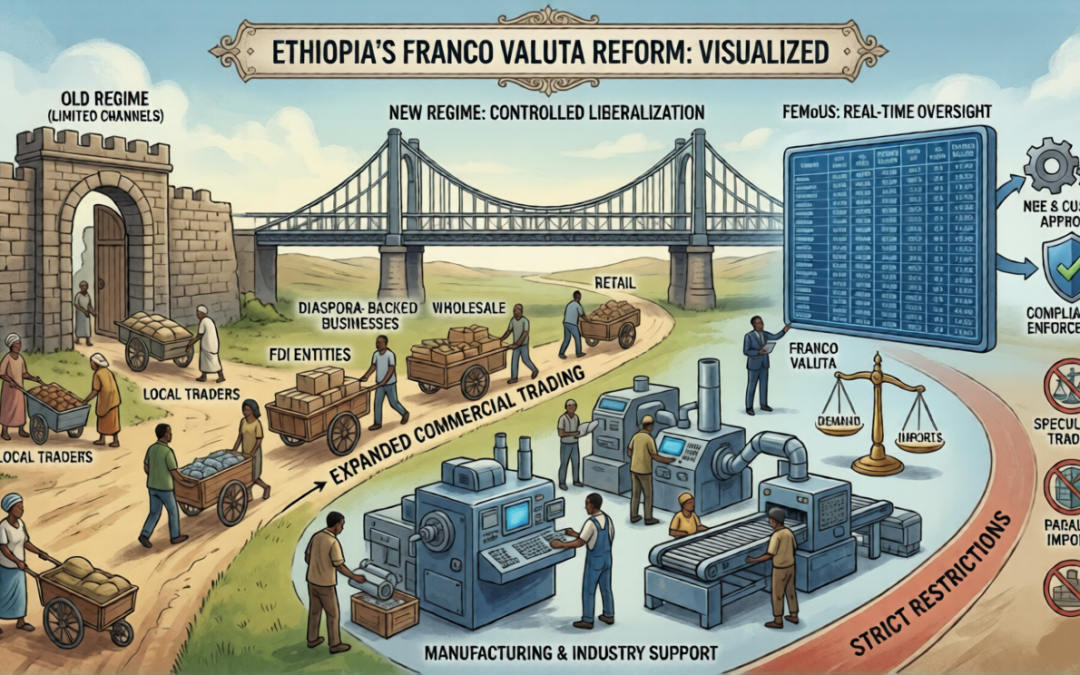

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

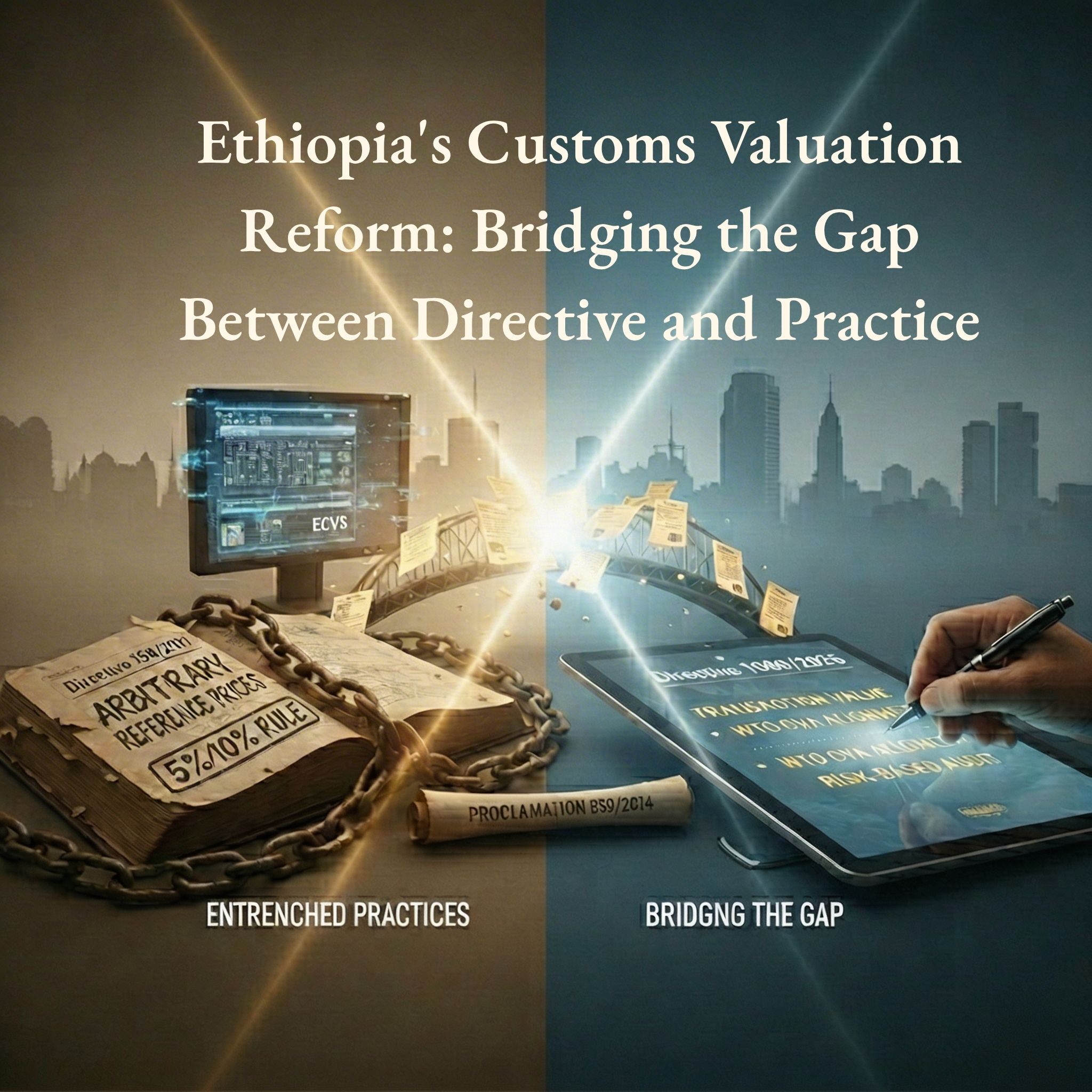

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.

U.S. International Tax Law in a Coffee Bean

The highlands of Ethiopia are widely regarded as the birthplace of coffee. The story of Ethiopian coffee dates back to around 850 AD, when both Arabica and Robusta coffee are believed to have originated. Today, Ethiopia remains the top coffee producer in Africa, cultivating over 5,000 varieties. Coffee is a major global export for the country, where agriculture remains a key driver of the economy. Ethiopia also ranks first in wheat production and third in maize production across Africa.