Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Introduction

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Against the backdrop of foreign exchange reform and ongoing IMF engagement, Ethiopia has introduced Customs Valuation Directive No. 1080/2025 with the stated aim of aligning national practice with international standards, particularly the WTO Customs Valuation Agreement. This reform raises a critical question for policymakers, investors, and importers alike: Does the new directive meaningfully address the entrenched practical problems of arbitrary valuation, or does the gap between legal intent and administrative practice persist ? This article examines whether Ethiopia’s latest customs valuation reform truly promotes fair market value, legal certainty, and investment confidence or merely repackages old challenges under a new regulatory framework.

1. The Core Conflict: International Principles vs. Local Practice

For years, Ethiopia’s customs valuation system has been a major point of contention for importers and investors. At the heart of the debate is a conflict between international standards and domestic directives that many argue distort market prices.

The International Standard: The World Trade Organization’s (WTO) Customs Valuation Agreement (CVA) establishes the transaction value—the price actually paid or payable for goods—as the primary basis for valuation. Rejecting this price should be the exception, not the rule.

The Old Ethiopian Practice (Directive 158/2011): A key provision, Article 5(2)(D), created an automatic rejection mechanism. If an importer’s declared price deviated by more than 5% (or 10% for manufacturers) from a price in the government’s Electronic Customs Valuation System (ECVS) database, the commercial invoice was rejected. This practice, which is used in nearly 90% of valuation decisions, often disregards actual market transactions. It creates an unrealistic burden on importers to estimate the “correct” database price for customs duty and tax purposes. Even after the release of goods, customs authorities can conduct audits for up to five years from the date of the customs declaration. During these audits, they may impose interest and penalties on imports based on the ECVS price.

2. The Ripple Effect: How Customs Valuation Hurts Business

The impact of this system extends far beyond the port, creating a cascade of challenges:

· Distorted Domestic Pricing: Under VAT and tax laws (Proclamation 1341/2024 and bookkeeping directive no 176/2014), if an importer declares the cost of sold goods less than the customs value, tax authorities can use the customs value for tax calculations. This means a good market price can be lower than its official customs value, making businesses uncompetitive and squeezing profits.

· Operational Struggles: Many investors report severe business challenges and difficulty sustaining operations because their actual costs and market realities are not aligned with the state’s valuation figures; in addition to custom tax and duty, they will pay high direct tax.

· According to the NBE circular, banks must use the custom price as the standard when allowing the opening of letters of credit (LC) for imported goods. As a result, there is a likelihood that the opening of an LC may be prohibited if the transaction value (fair market value) is either higher or lower than the customs price.

3. The Reform Effort: Directive 1080/2025

Recognizing these systemic issues, the Ministry of Revenues issued a new Customs Valuation Directive No. 1080/2025. This directive represents a significant theoretical overhaul aimed at fixing past problems:

· Explicit Alignment: It explicitly aims to align Ethiopia’s system with international principles and agreements, including the WTO CVA.

· Broader Scope & Clarity: It moves beyond narrow valuation methods to cover pre- and post-clearance controls, related-party transactions, and digital systems.

· Formal Structure: It properly sequences valuation methods, mandates justification for rejecting transaction value, and details factors affecting value (like buyer-seller relationships).

· Improved Enforcement: It introduces risk-based mechanisms and stronger audit powers, shifting towards proactive compliance.

4. The Persistent Gap: Theory vs. Practice

While Directive 1080/2025 is a major structural upgrade on paper, significant practical challenges remain:

a. Deep-Rooted Practices: The old, database-driven comparison method is a “long-lived tradition” that is difficult to eradicate overnight. Customs officers may still default to familiar practices.

b. Administrative Capacity: Implementing the new directive’s principles—like detailed comparability analyses—requires training and resources that may be in short supply.

c. The Shadow of the ECVS: The legacy of the arbitrary 5%/10% rule from the old system casts a long shadow, and importers remain wary.

5. The Broader Context: A System Under Scrutiny

This reform is happening within a pressurized environment: the International Monetary Fund (IMF) is evaluating Ethiopia’s systems as part of broader foreign exchange policy changes.

Following the enactment of the directive, the National Bank of Ethiopia (NBE) recently mandated banks to use a “custom price” for Letters of Credit for certain goods, highlighting ongoing state intervention in pricing.

The core legal conflict between old directives and the overarching Customs Proclamation No. 859/2014 (which itself aligns with WTO principles) has created years of legal uncertainty.

Conclusion: A Step Forward, But the Journey Continues

Ethiopia’s Customs Valuation Directive 1080/2025 is a clear and necessary step toward a fairer, more predictable, and internationally compliant trade system. Structurally, it largely meets global standards.

However, the true test lies in implementation. For importers and investors to feel real change, the deeply ingrained practice of arbitrary database comparisons must end. The government’s commitment will be measured not by the text of the new directive, but by its success in retraining its administration, building capacity, and consistently applying the principle that the real price paid between a buyer and a seller is the primary basis for value, not a number in a government database. Until then, a gap between promising theory and difficult practice will remain.

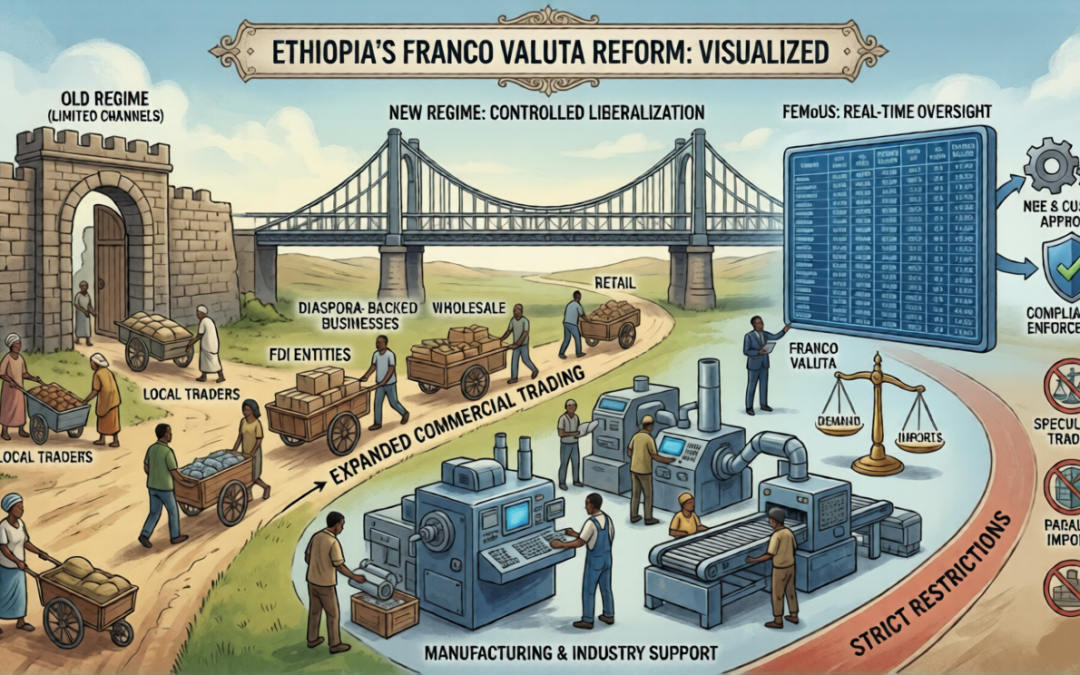

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

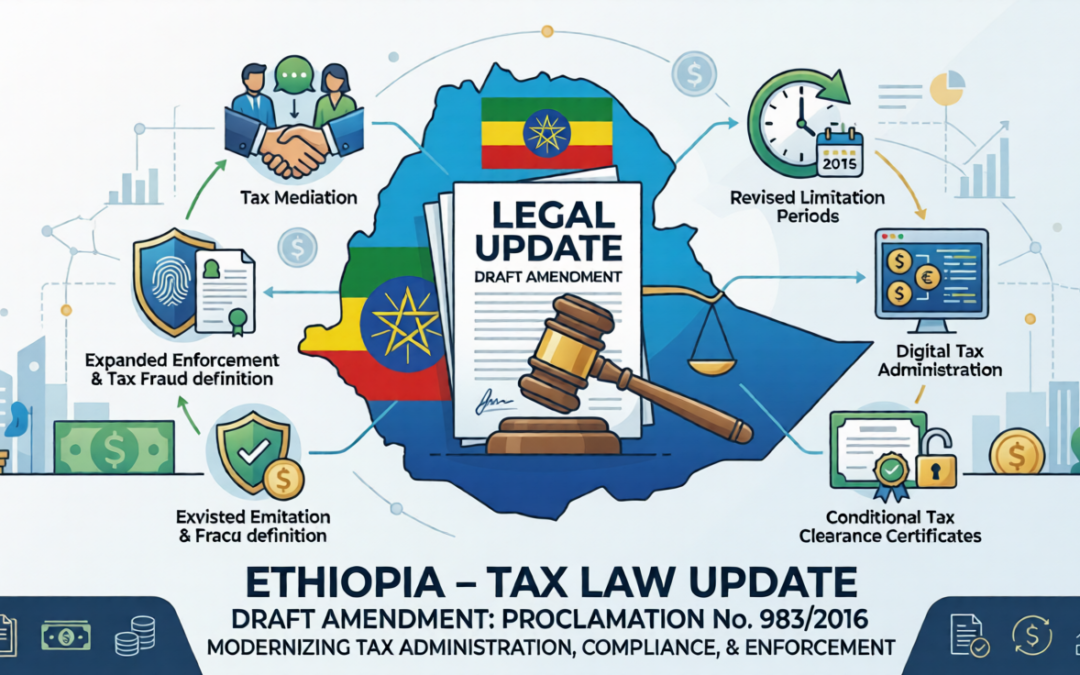

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

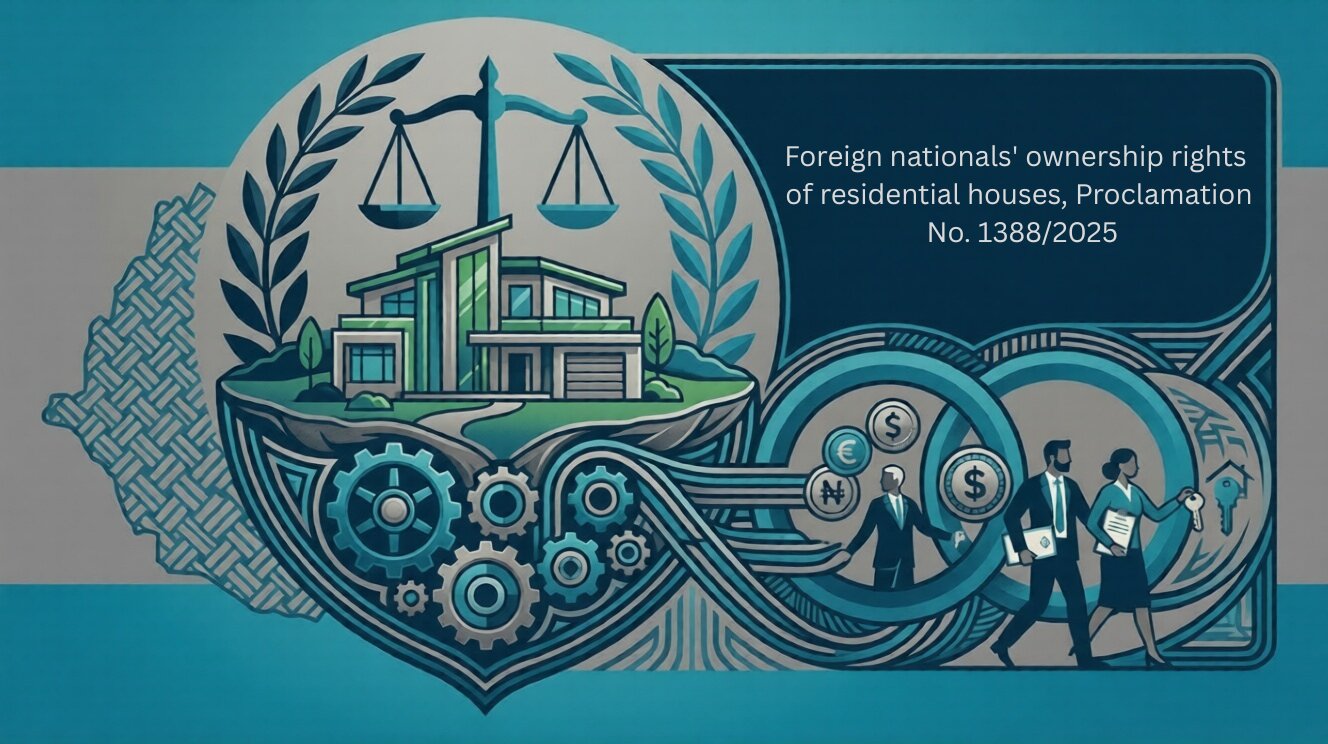

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.

U.S. International Tax Law in a Coffee Bean

The highlands of Ethiopia are widely regarded as the birthplace of coffee. The story of Ethiopian coffee dates back to around 850 AD, when both Arabica and Robusta coffee are believed to have originated. Today, Ethiopia remains the top coffee producer in Africa, cultivating over 5,000 varieties. Coffee is a major global export for the country, where agriculture remains a key driver of the economy. Ethiopia also ranks first in wheat production and third in maize production across Africa.