Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

Under the newly issued notice on relaxation of foreign exchange directive (hereinafter referred as “ the Notice”) , one of the most notable changes is the removal of the previous minimum requirement of USD 100,000 to open a foreign currency savings account for resident and non-resident Ethiopians. This reform substantially broadens access to foreign currency banking services, promotes financial inclusion, and is expected to encourage greater formalization of foreign currency holdings within the banking system.

The Notice also introduces important developments concerning outbound investment. It is widely recognized that many Ethiopian individuals and companies incorporated in Ethiopia have long sought to expand their commercial activities beyond national borders. Historically, regulatory constraints, particularly foreign exchange shortages and strict approval procedures, posed significant barriers. The new framework now permits outbound investment, subject to prior approval from the NBE. This marks a meaningful shift toward outward economic engagement and signals the regulator’s confidence in the evolving stability of the forex market.

Another major reform concerns foreign currency conversion. Individuals residing in Ethiopia are now permitted to convert foreign currency holdings through banks or authorized foreign exchange bureaus without the requirement of presenting a customs declaration. This measure simplifies compliance requirements, reduces administrative burdens, and enhances the liquidity of foreign currency circulating within the formal financial sector.

The Notice further relaxes outbound remittance rules. Foreign currency account holders may remit up to USD 3,000 abroad. For individuals without foreign currency accounts, outbound remittances remain permissible subject to the submission of supporting documentation, thereby maintaining regulatory oversight while improving flexibility.

In a significant move toward market liberalization, commercial banks are now authorized to enter into forward foreign exchange transactions without seeking prior approval from the NBE. This development is expected to deepen the foreign exchange market, enhance risk management mechanisms for businesses, and support more sophisticated financial operations, particularly for importers and exporters exposed to currency fluctuations.

Exporters also benefit from enhanced flexibility. They are now permitted to receive advance payments from buyers, provided that the terms and conditions are contractually agreed upon. Moreover, exporters may accept payments for future exports as long as such payments are clearly designated as advance payments and properly reference the type of commodity, invoice number, or contract number. This reform is likely to improve exporters’ working capital positions and strengthen trade competitiveness.

Banks are now allowed to guarantee private external loans, provided that the guarantee does not exceed ten percent of the company’s capital. This measure facilitates access to external financing while prudently managing systemic risk exposure within the banking sector.

Importantly, the Notice confirms that investors may repatriate dividends or net profits without obtaining prior NBE approval, provided that all regulatory requirements are fulfilled. This reform is particularly significant for foreign direct investment (FDI), as ease of profit repatriation is a critical determinant in investor decision-making and long-term capital commitment.

Finally, the cash holding limit for independent foreign exchange bureaus has been increased from 10 percent to 25 percent of their capital. Any excess beyond this threshold must be sold to commercial banks. This adjustment enhances operational liquidity for forex bureaus while ensuring that excess foreign currency is channeled back into the formal banking system.

Collectively, these measures reflect a deliberate and structured transition toward a more liberalized and market-responsive foreign exchange regime. While regulatory oversight remains in place, the direction of reform clearly signals Ethiopia’s broader commitment to financial sector modernization, improved investor confidence, and deeper integration into the global economy.

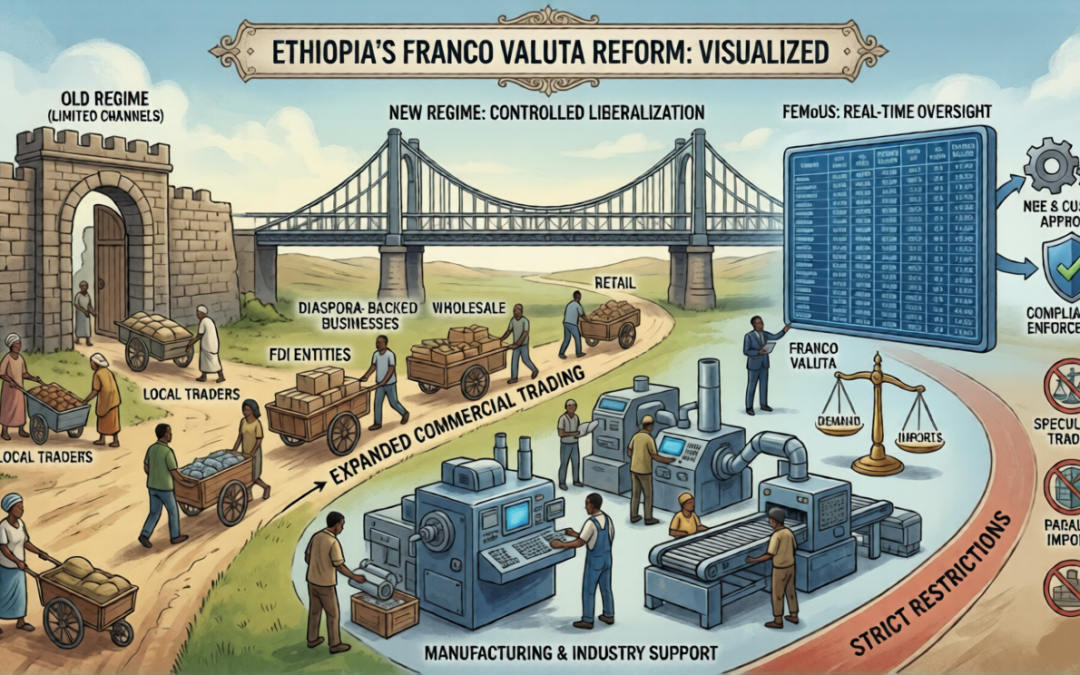

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

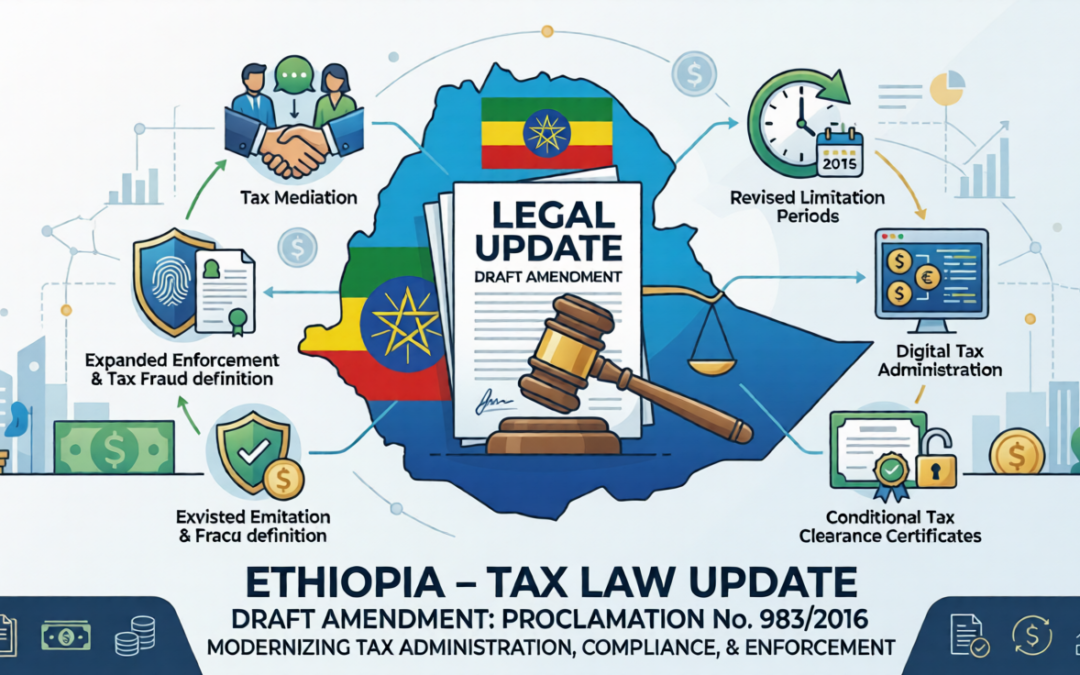

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

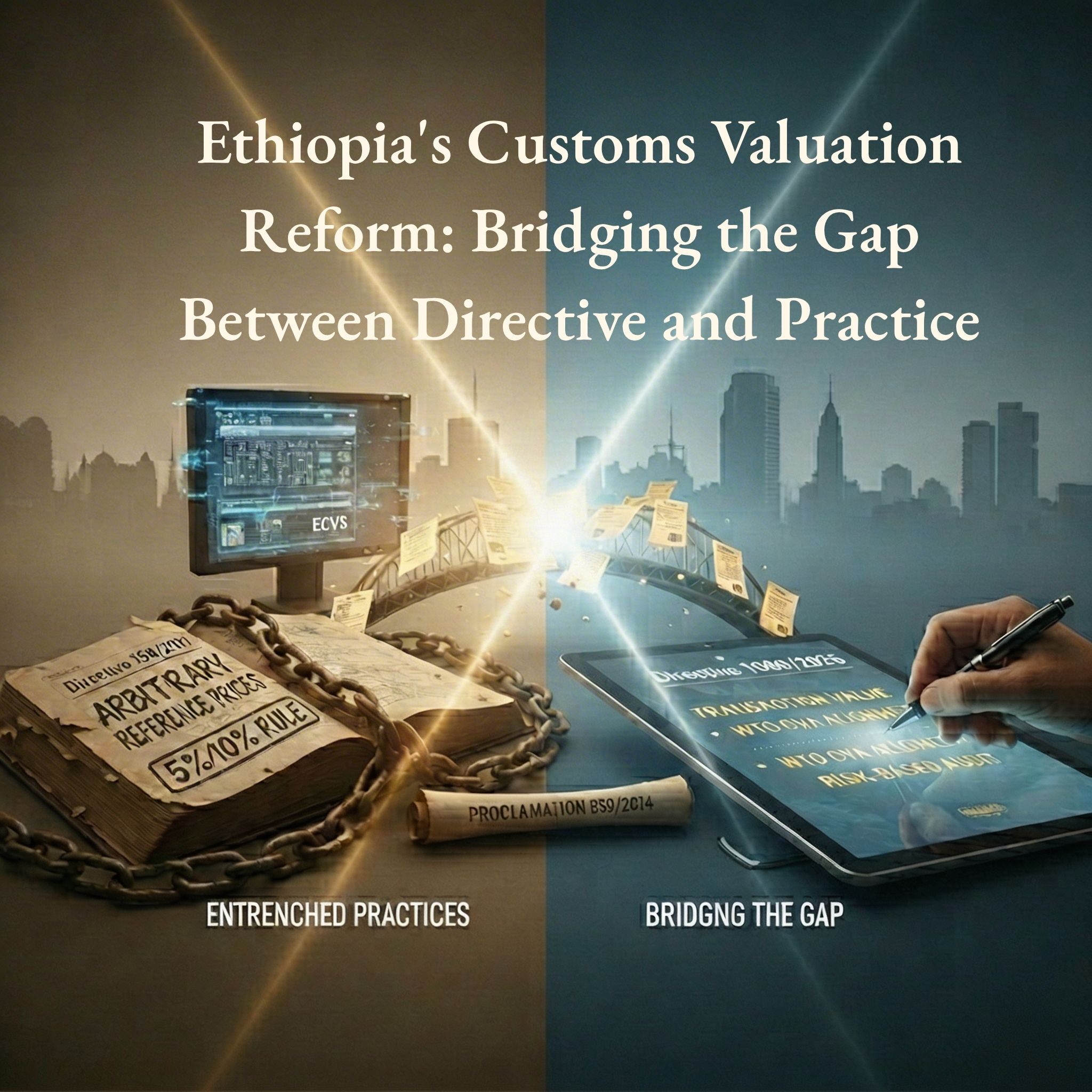

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

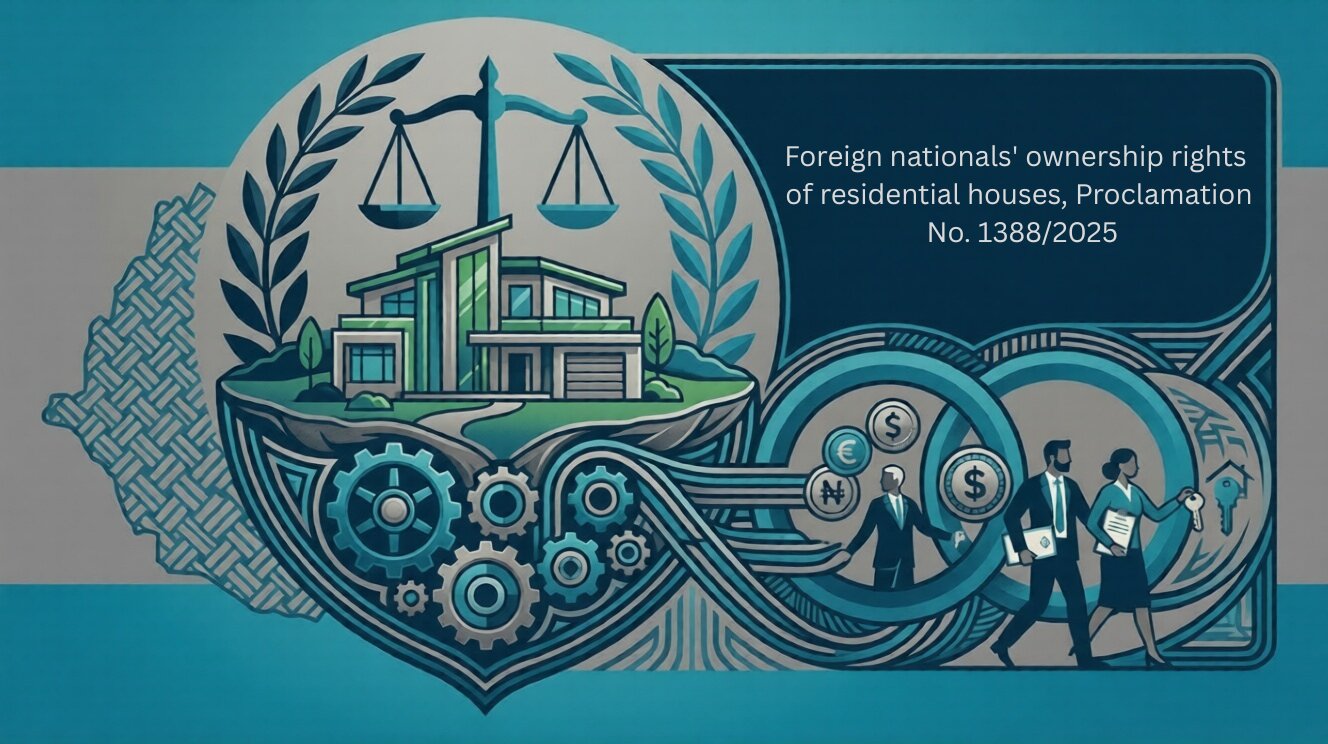

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.

U.S. International Tax Law in a Coffee Bean

The highlands of Ethiopia are widely regarded as the birthplace of coffee. The story of Ethiopian coffee dates back to around 850 AD, when both Arabica and Robusta coffee are believed to have originated. Today, Ethiopia remains the top coffee producer in Africa, cultivating over 5,000 varieties. Coffee is a major global export for the country, where agriculture remains a key driver of the economy. Ethiopia also ranks first in wheat production and third in maize production across Africa.