Dispute over Taxing Undistributed Profit in the Context of Tax Treaties

- Highlight on Background of Taxing Undistributed Profit.

Taxing undistributed profit of companies, more numerously PLCs in Ethiopia, has for a long time been the reason for complaints and proceedings within the tax dispute resolution system. In 2013 the then Revenues and Customs Authority noticed that most PLCs were not paying tax on dividends. But the PLCs challenged authority that they are obliged to pay tax on dividends only when the dividend is paid to shareholders. Furthermore, they argued that imposing tax on undistributed profit is equivalent to levying tax without law enacted by the parliament, the only branch of government entrusted with the power to levy tax. Thus, they contended that imposing a tax on undistributed dividends is essentially levying tax without legal grounds, which violates the principle of the legality of taxation.

The authority however, continued pressure on taxpayers to collect the tax from undistributed profit considering it as dividend. It is Ministry of Finance that tried to solve the issue partly by lifting the interest and penalty and wrote circular which provides an option for tax payers either to increase capital using undistributed profit or pay principal tax if they choose to distribute the dividend or fail to fulfill the conditions required by the ministry of finance. Conditions set in the circular of the ministry are producing document adducing undistributed profit is used for capital increment and after 2014 tax year the taxpayers are required to increase their capital from dividend within 12 months after the budget year. This fact also has to be reported to the then revenues and customs authority according to the circular.

Tax payers were challenging the circular until income tax proclamation No. 979/2016 was enacted. The argument from the side of taxpayers was that income tax proclamation No. 286/2002 does not have mandatory provision obliging taxpayers to pay dividend on undistributed profit. Thus, they considered it as imposing tax without legal provision obliging to do so.

The tax authority continued its pursuit, despite the new income tax proclamation specifically mandating taxation of undistributed profit as dividend, affirming the argument raised by taxpayers.

The taxpayers continued to contest the authority’s decision, arguing that the tax authority lacks the jurisdiction to enforce taxation on undistributed profit prior to the issuance of the new income tax proclamation. They maintained that the explicit provision by the lawmaker indicates that the previous proclamation did not mandate taxpayers to pay tax on undistributed profit. Consequently, they assert that the tax on undistributed profit is being introduced for the first time by the new income tax proclamation. But now the dispute over undistributed profit based on previous income tax proclamation ended as time for amending tax notice for tax years before 2016 is lapsed.

The ongoing dispute primarily was concerned with legality of imposing such a tax. Now the new proclamation, as mentioned above, explicitly provided for taxation on undistributed profit unless taxpayers reinvest undistributed profit in accordance with the directive issued by Ministry of Finance. Accordingly, Ministry of Finance Issued Directive No. 7/2011 which under article 5 provides that undistributed profit is taxable by the rate of 10% unless taxpayer has reinvested it within 12 months from end of tax year. It requires taxpayers to get the minute increasing the capital of the company authenticated by relevant authority entrusted with power to authenticate contracts and the amount of capital increased must be reflected in trade license issued by relevant authority. Unless these requirements are fulfilled within specified time limit it is considered that the company waived its right to use undistributed profit for increment of capital.

- Payment of Dividends as Prerequisite under Double Taxation Avoidance Treaties

Certainly! One of the key aims of double taxation avoidance treaties is to create a conducive environment for investment by providing certainty for taxpayers from their home country. One way of accomplishing this is by complying with the terms of the treaty, which could effectively avoid disputes.

The issue of undistributed profit is clear when it comes to companies established by domestic investors. However, the question pertains to applicability of the income tax proclamation’s provision for the taxation of undistributed profits in the context of double taxation avoidance treaties, which necessitate the payment of dividends. At this juncture it is important to produce a provision dealing with dividends from double taxation avoidance treaty between China and Ethiopia to demonstrate requirement of payment for dividend to be taxed. Article 10(1) and 10(2) of treaty reads as follows:

10(1) “Dividends paid by a company which is resident of a contracting state to a resident of other contracting state may be taxed in that other state”

10(2) “However, such dividends may also be taxed in the contracting state of the company paying the dividends is resident…”

The provision highlights taxation of dividends when payment of such dividend is made to the recipient. The term “paid” has an extensive meaning as it signifies the fulfillment of the obligation to allocate funds to the shareholder in the manner stipulated by contract or customary practice. Consequently, the tax authority is mandated to ensure that the payment has been duly made to the recipient. This definition could be helpful when the tax authority applies terms of income tax proclamation to entities established or carrying on business from countries having DTTs with Ethiopia.

The practice however, shows the other way round. Companies established by investors from countries having double taxation avoidance treaties are now required to pay tax on undistributed profit despite clear provision in double taxation avoidance treaty between Ethiopia and their home countries. This could create challenges for companies established by investors from countries with such treaties. It’s important to address this issue and ensure that the implementation aligns with the provisions outlined in the relevant double taxation avoidance treaties.

The applicability of article 61 of income tax proclamation No.979/2016 is limited to taxpayers that are not covered double taxation avoidance treaties. The tax on undistributed profit is not a tax of different nature though it appears to be. It is tax on profit which could have been distributed as dividend. In that case tax on dividend that is not paid is not subject to tax where the entity having such undistributed profit is established by foreign investors from countries having double taxation avoidance treaties with Ethiopia as it is clearly provided under treaties that tax is paid when dividend is paid to shareholders. It should be understood so because it is clearly provided under article 48 of income tax proclamation that if there is any conflict between terms of treaty and the provisions of the proclamation, the terms of treaty prevails over the provisions of proclamation. Therefore the tax authority should take into account of the provisions of treaties the country signed when applying provisions of proclamation.

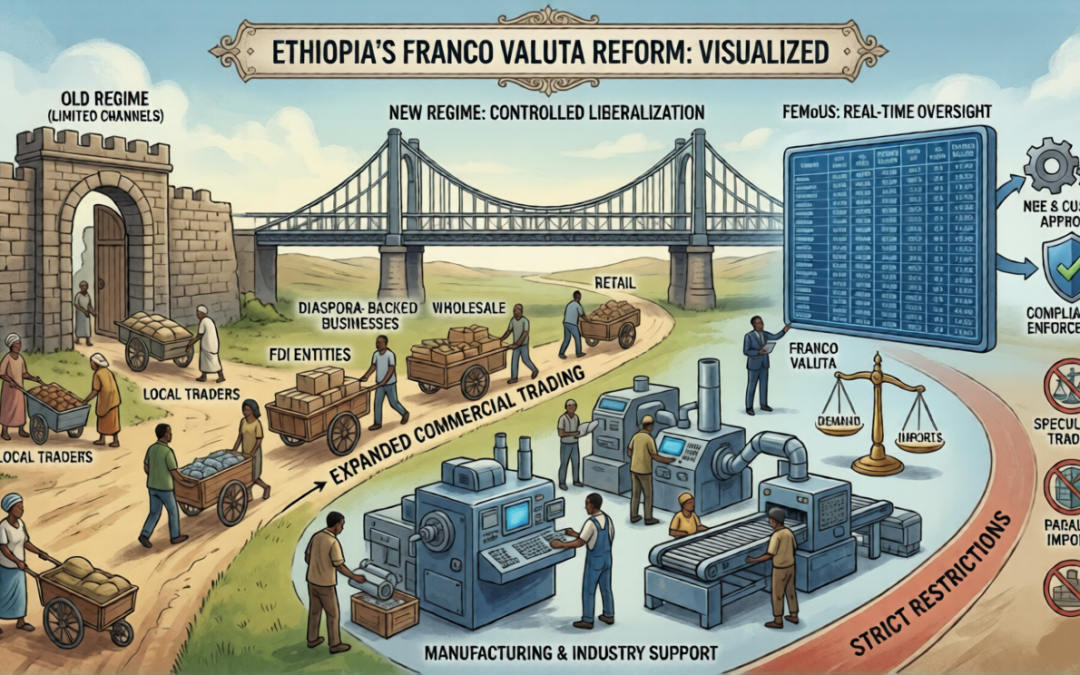

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

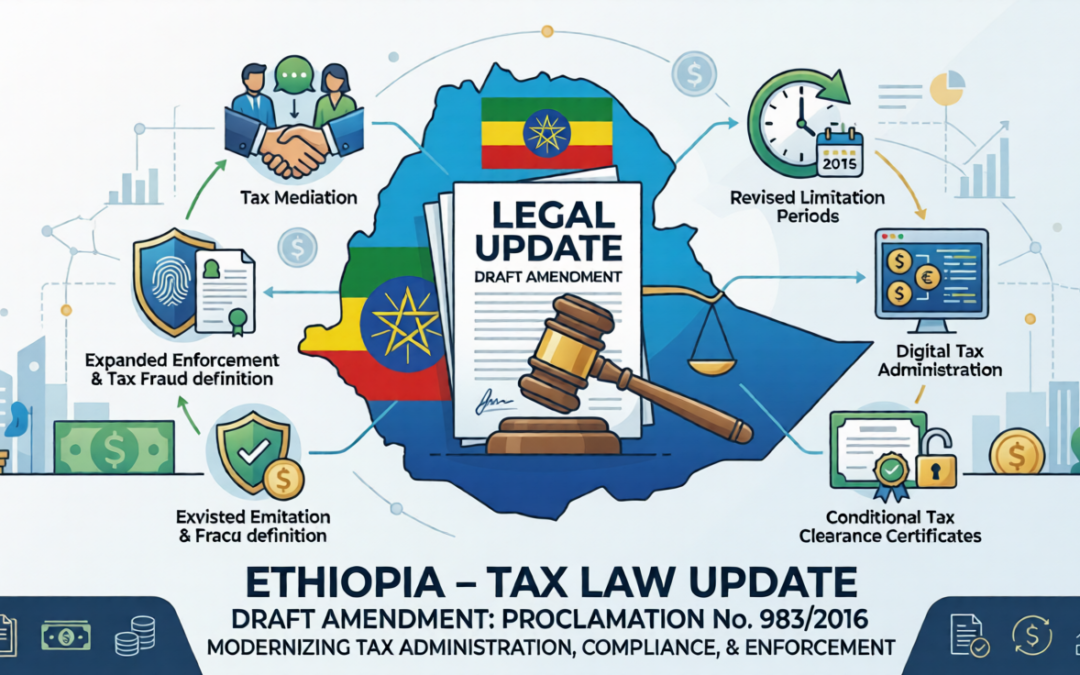

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

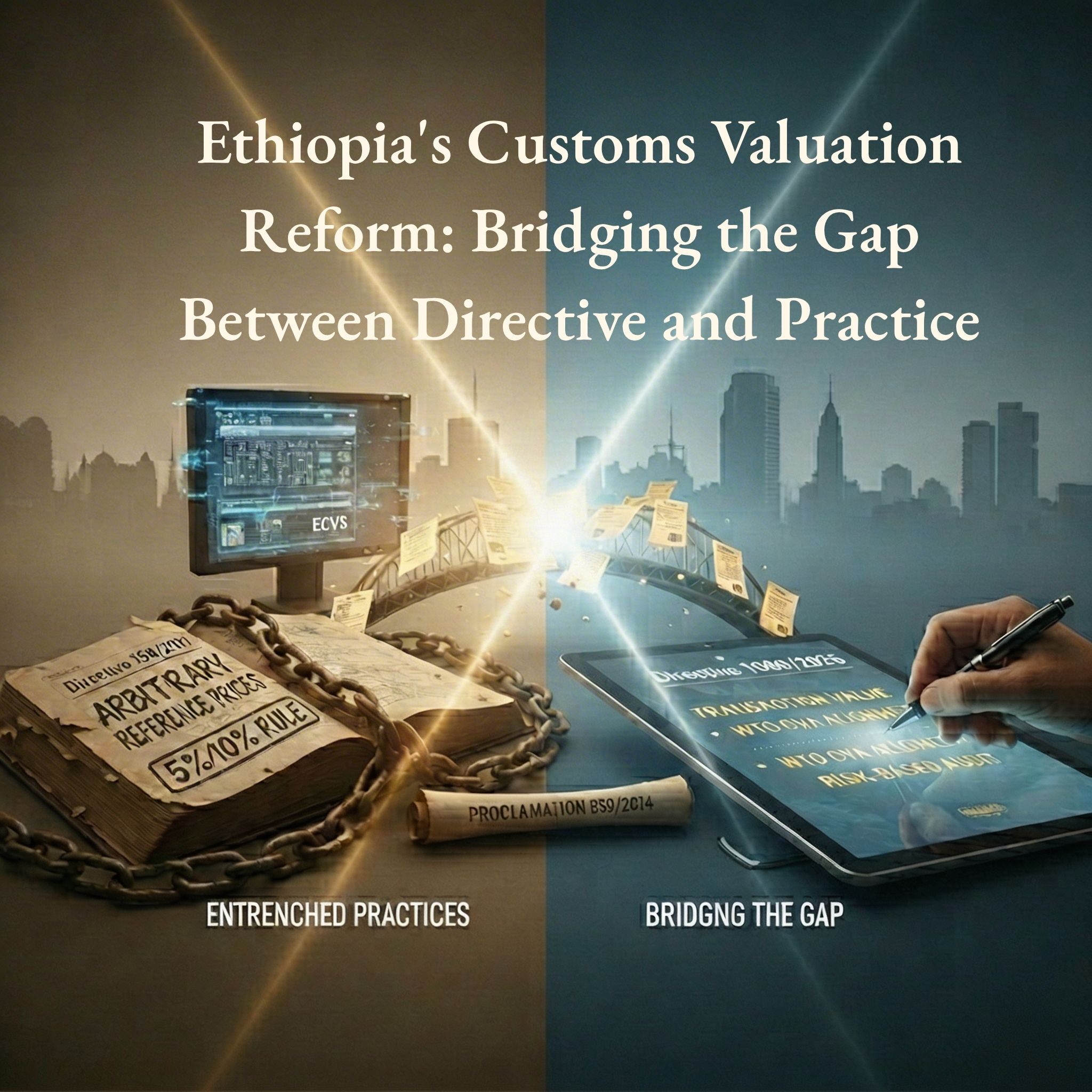

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

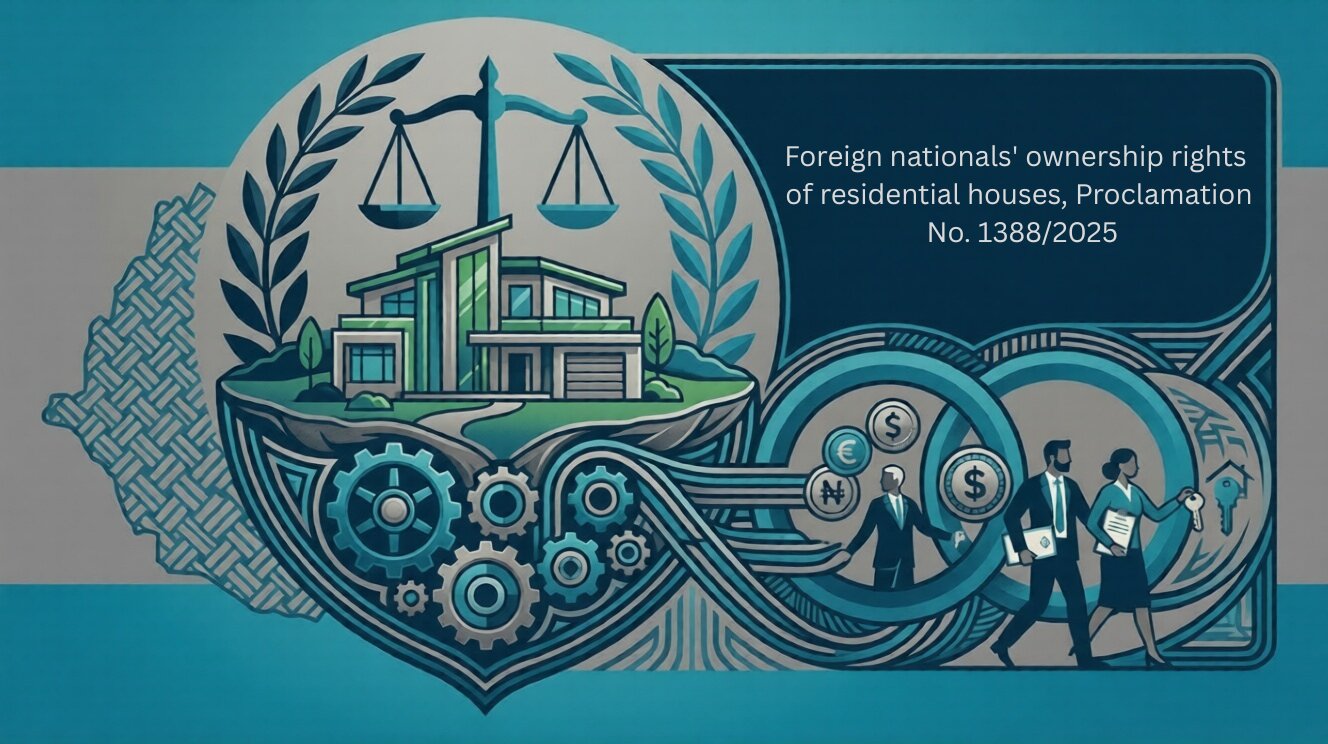

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.