The Dream and the Dilemma of Africa’s Single Currency

It is an ambitious plan that sees the African Union (AU) striving to create a single currency for the continent, marking a crucial part of its economic integration strategy. The initiative, crafted within the broader design of the Abuja Treaty of 1991, aspires to pool regional economic communities (RECs) or blocs into a unified African customs union and create an African Central Bank, issuing the single currency – the Afro or Afriq – by 2025.

A monetary unification of this magnitude has its potential rewards but also poses significant challenges.

The groundwork is being laid through building blocks of monetary unions within five key economic communities: the West African Economic & Monetary Union (WAEMU), the Economic & Monetary Community for Central Africa (CAEMC), the Arab Monetary Union (ArMU), the Southern African Monetary Union (SAMU), and the East African Monetary Union (EAMU), all under the umbrella of the proposed African Monetary Union (AMU).

The West African and Central African regions currently use the French Franc, fostering seamless intra-regional transactions. However, friction arises when transactions span across different communities.

The scenarios to address this challenge broadly fall into three categories.

The first is facilitating intra-bloc transactions like domestic ones, reducing currency exchange risk. In essence, this scenario bypasses the difficulties of cross-regional transactions by enhancing trade within a singular currency area. It is a safe strategy, guarding against price instability and financial crises.

A more complex scenario envisions transactions between two different blocs. Imagine a merchant in Gabon (CAEMC) importing a car from Kenya (EAMU). The payment might be made in Francs but eventually converted to Dollars for the Kenyan trader. This scenario’s inner workings reveal a tricky situation. The CAEMC Central Bank, although appearing to function normally as it exchanges Francs for Dollars, in reality, exhausts its reserves in the process.

It is left with the power to regulate and issue Francs, but without the Dollar reserves, the Bank cannot effectively control price stability and ensure the smooth functioning of interbank exchanges. This could lead to a vicious inflationary cycle, with constantly rising prices and a steady local currency devaluation.

The last scenario envisions an optimistic future of a unified African currency, mandating a supranational organization to handle the monetary policies of member states. It would act as a control mechanism over member states, potentially eliminating macroeconomic uncertainty and inviting foreign direct investment.

Proponents of the single currency project often highlight three primary benefits: low inflation, economic growth, and greater unity among African nations.

Indeed, the single currency might boost intra-African trade, a fact supported by studies indicating that countries sharing a common currency trade three times more than those with different currencies. The AU may use the single currency as an instrument to ensure stability and ward off financial and economic aggressions. This could also reinforce Africa’s ability to handle internal conflicts, uphold democracy, and strengthen the continent’s position on the global stage.

Simple, it may seem, but complexities abound when one delves into public spending. Members of a single currency union enjoy reduced transaction costs, price transparency, and the elimination of exchange rate uncertainty, to name a few. However, the costs of the union come into play when considering the sovereignty over a monetary policy that countries would have to forfeit. Especially if the shocks affecting the economies are asymmetric, the cost of joining a single currency union can be pretty high.

Countries with fiscal imbalances due to inefficient tax collection or excessive public sector spending could exert pressure on central banks to finance the deficit, potentially leading to inflationary pressure. The tension could also extend to commercial banks, which might be forced to lend to state-owned enterprises without proper safeguards, leading to a mounting pile of bad debts and raising the speculation of potential bank failures. Such a scenario occurred in the 1980s in the Communauté Financière Africaine (CFA) zone.

Many African countries, which may not be particularly competitive and may have inflexible labour markets or excessive private and fiscal debt, could face liquidity issues, leading to sovereign risk in the financial system. While a single currency might initially offer a boost in trade and promote economic unity, the risks inherent to its implementation could lead to monetary instability and a resultant economic fallout.

African Continental Free Trade Area (AfCFTA) is an ambitious project that could reshape the continent’s economic landscape. Yet, as with any significant monetary endeavour, it carries a risk. If not handled meticulously, the one-currency utopia could turn into a devastating whirlpool of economic instability.

While a single African currency may indeed offer many benefits, such as boosting trade, lowering inflation, and fostering unity, the risks and complexities involved in its implementation demand careful consideration. Africa’s leaders will need to balance these risks with the potential benefits and have in place robust strategies to deal with the potential challenges that could arise.

Essentially, the dream of a single African currency is tantalizing, promising increased intracontinental trade and unity. But as the old saying goes, the devil is in the details. And in this case, the details are knotty and complex, requiring careful navigation and cautious implementation. A crucial factor is managing the economic disparities and diverse fiscal policies across member states. Creating a unified economic and monetary policy to cater to nations with varied levels of economic development, political stability, and fiscal discipline would require extraordinary consensus-building and diplomatic skills.

An institutional design will be paramount in achieving a monetary union. The European Union’s eurozone provides both a blueprint and a cautionary tale. Establishing a supranational entity like the European Central Bank has primarily worked to maintain price stability, but the lack of a unified fiscal policy has led to significant challenges, particularly in times of economic crisis. This dichotomy is something Africa’s policymakers must consider as they plan the African Central Bank (ACB).

Another concern lies in the potential for larger economies to dominate the union at the expense of smaller ones. Economically dominant countries may sway monetary policy to their advantage, leaving less prosperous countries on the economic back foot. This requires a fair system where influence in the ACB reflects the economic reality but does not create an inequitable balance of power.

On the positive side, the single currency could serve as a platform for Africa’s voice in global economic forums, giving the continent a stronger bargaining position on international trade deals and enabling collective resistance against economic exploitation.

The vision of a single currency for Africa is indeed a grand one. However, the journey is fraught with considerable challenges, from managing inflationary pressures and maintaining fiscal discipline to balancing the needs of diverse economies and ensuring a fair system of influence in the African Central Bank. It is an economic tightrope walk where careful planning and well-executed strategies are crucial. The hope is that Africa’s leaders, guided by lessons from other monetary unions and armed with a clear understanding of the potential pitfalls, can guide the continent towards successful monetary integration.

The views and opinions stated in this article are solely the author’s and do not represent the institutions or projects he is affiliated with.

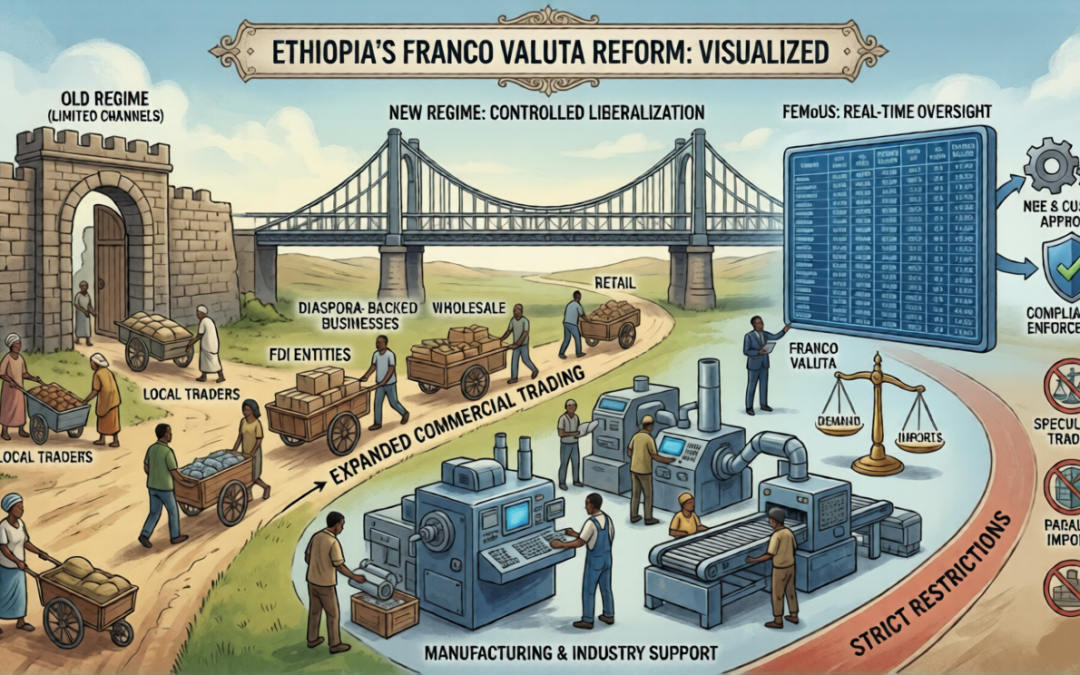

Ethiopia’s Franco Valuta Reform: Expanded Import Channels with Targeted Restrictions on Trading and Manufacturing

Businesses that combine strategic structuring with rigorous compliance will be best positioned to unlock the full commercial value of Franco Valuta.

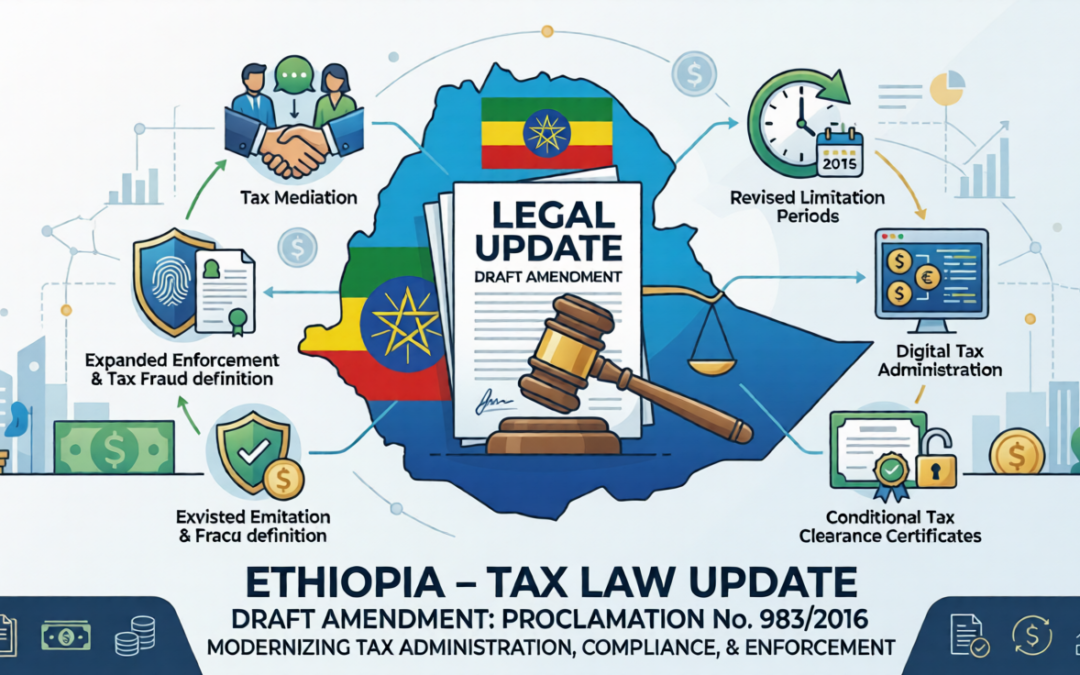

Draft Amendment to the Federal Tax Administration Proclamation No. 983/2016

The Federal Democratic Republic of Ethiopia has introduced a draft amendment to the Federal Tax Administration Proclamation No. 983/2016, which establishes the legal framework governing tax administration, compliance, enforcement, and dispute resolution in Ethiopia.

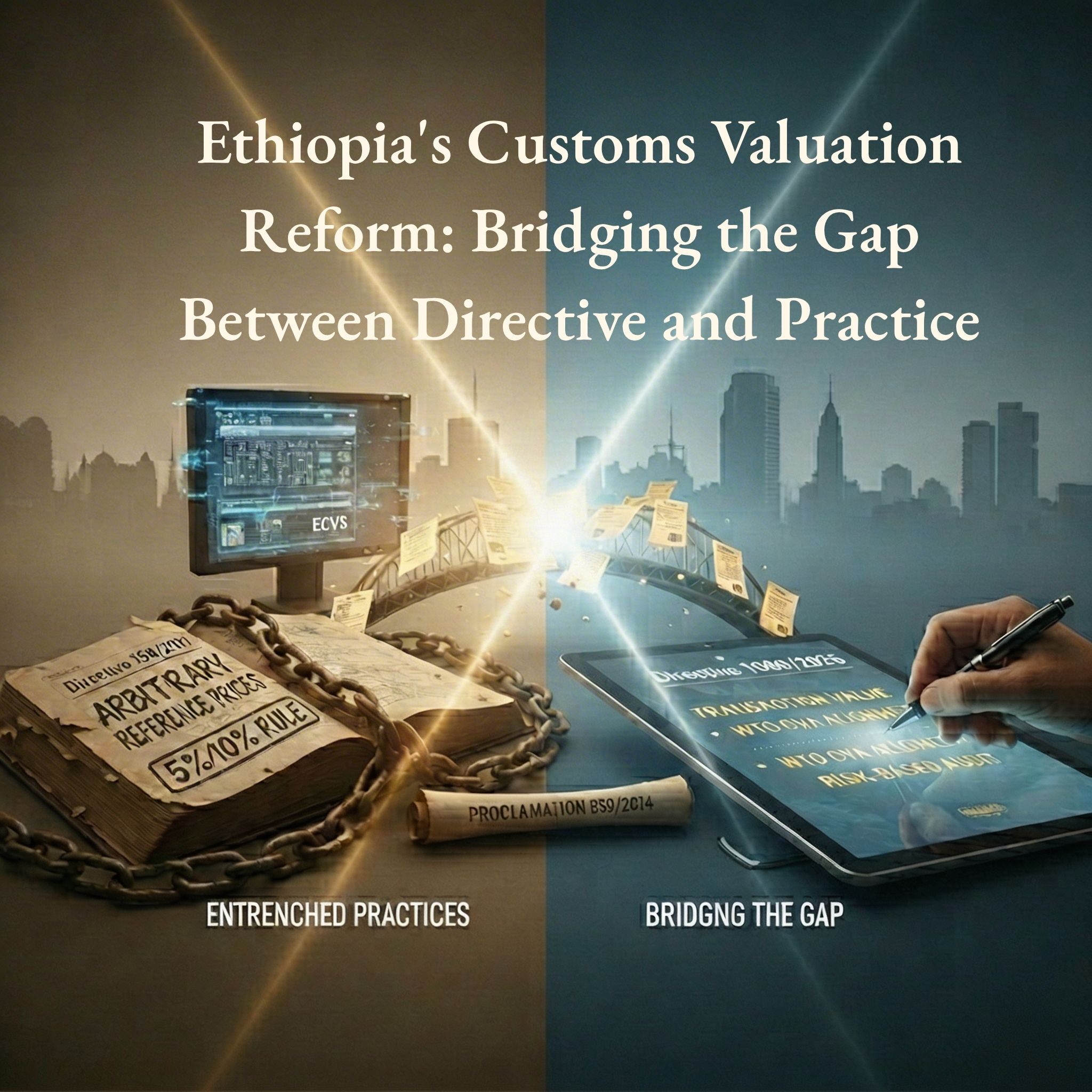

Ethiopia’s Customs Valuation Reform: Bridging the Gap Between Directive and Practice

Customs valuation has long stood at the centre of Ethiopia’s trade, investment, and foreign exchange challenges. While revenue protection and foreign currency control remain legitimate state objectives, the persistent reliance on arbitrary reference prices—particularly under Customs Valuation Directive No. 158/2011—has created serious distortions in trade administration, banking operations, and domestic taxation. The recent circular issued by the National Bank of Ethiopia on January 26, 2026, requiring banks to use customs prices as a reference for Letters of Credit, has once again brought this debate to the forefront, exposing the far-reaching consequences of valuation practices that diverge from internationally accepted principles.

Legal Opinion in Capital Markets: Standards, Independence, and Verification

A) Why Legal Opinion?

Lawyers are envisaged to play pivotal roles in capital market especially in security registration.

Investor Protection: Legal opinions often assess existential risks like litigation, asset ownership, and regulatory compliance. A biased opinion could mislead investors.

Market Integrity: Capital markets rely on trust. Conflicted legal opinions undermine transparency and fairness.

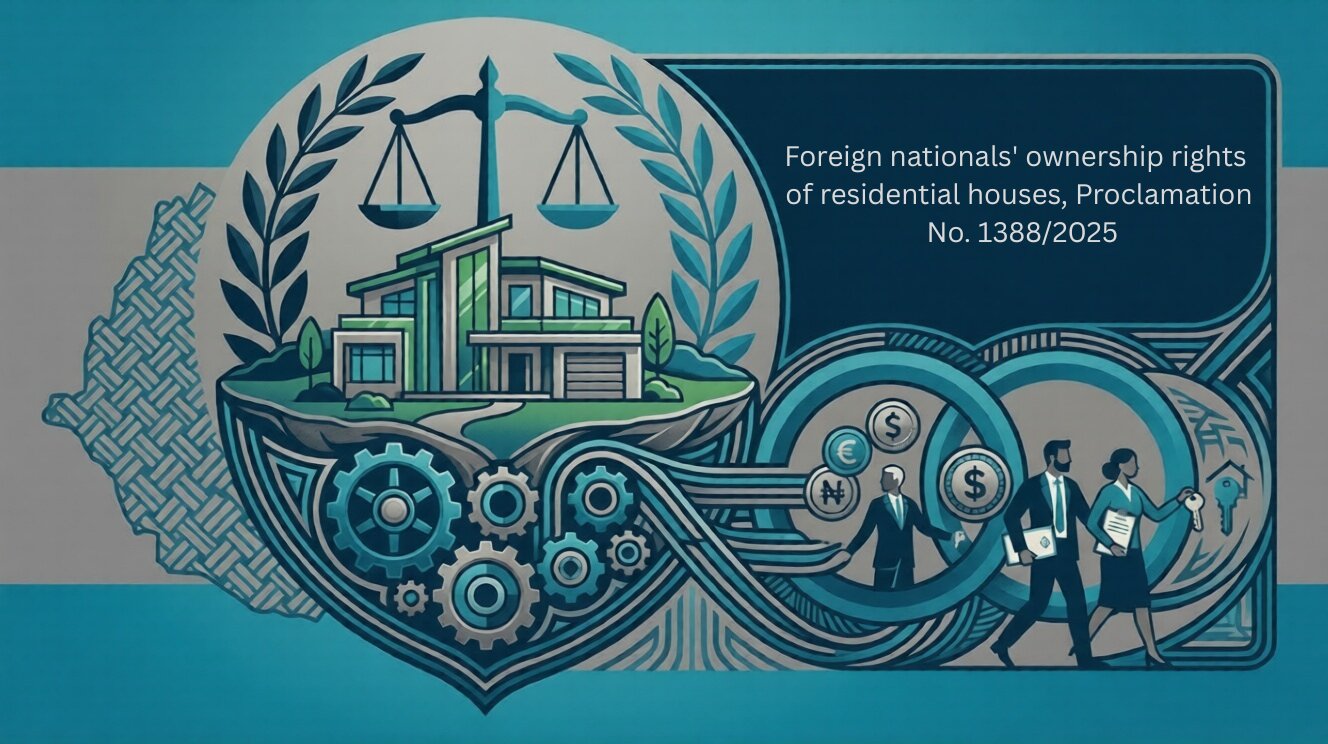

Foreign national’s ownership rights of residential houses, Proclamation No. 1388/2025

The ownership rights of foreign nationals over residential houses are governed by Proclamation No. 1388/2017. The proclamation consists of twenty-one (21) articles organized into four sections.

Ethiopia’s Investment Incentive Reform 2026: Key Legal Shifts from Regulation 517/2022 to 586/2026

Ethiopia has significantly revised its investment incentive regime with the replacement of Investment Incentive Regulation No. 517/2022 by the new Regulation No. 586/2026. This reform shifts the system from multi-year tax holidays and broad customs exemptions to a performance-based framework with targeted incentives. In essence, blanket income tax holidays are eliminated, replaced by reduced tax rates tied to priority sectors and performance, and new incentive categories (such as Special Economic Zones, start-ups, and green investments) have been introduced. The core customs duty benefits are largely retained but with refined conditions. This legal update outlines the key changes between the two regulations across five dimensions: tax incentives, customs duty incentives, administrative procedures, eligibility criteria, and sectoral priorities, and concludes with implications for investors and practitioners.

Legal Insight: New Developments in Ethiopia’s Foreign Exchange Framework

Following the comprehensive macroeconomic reform program, the National Bank of Ethiopia (NBE) has undertaken significant measures aimed at liberalizing the foreign exchange regime and fostering the development of a more efficient and market-oriented forex system. A central pillar of these reforms has been the gradual removal of current account restrictions and the introduction of regulatory flexibility designed to stimulate foreign exchange inflows, encourage investment, and enhance market confidence.

The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

By Kaleegziyabher Gossaye.

Legal update on The licensing and supervision of banking business reserve requirements (9th replacement) directive number SBB/97/2025

Risk Based Capital Adequacy Requirements for Banks-Directive No. SBB/95/2025

By Kaleegziyabher Gossaye.

The directive is organized into six parts. The first part outlines the general provisions of the directive. The second part deals with definition of capital. The third part discusses the capital requirements for credit risk. The forth and the fifth part extend to the capital requirements of market risks and operational risks. The last part, but not the least, is dedicated to miscellaneous provisions.

Ethiopia’s Amended Income Tax Proclamation: Implications for Revenue, Professionals, & Investors

The goals of the amendment are typically outlined in the preamble of the proclamation. Therefore, the objectives mentioned in the preamble include: improving revenue collection through adjustments to the rates applied to certain incomes; expanding the tax base; creating an efficient system of tax incentives; and curbing tax avoidance strategies, which encompass restrictions on cash payments.